¥/$ May Be Heading to ¥125

More in Japan Disagree with Kuroda That A Weak Yen is Good for Japan

¥125/$ is where the yen is headed to next, say a majority of currency forecasters. After weakening slowly since early 2021, the yen suddenly ratcheted—see figure above—after US Federal Reserve chair Jerome Powell indicated that he would raise interest rates even faster than expected, while Bank of Japan Governor Haruhiko Kuroda said the opposite. Kuroda said that Japan would continue its near-zero interest rate policy even if Japanese inflation temporarily hit 2%. That’s because Kuroda did not expect any such surge to last. In New York on March 24, the yen closed at ¥122.4. If it hits ¥125, that would be the weakest level in 20 years. Keep in mind that a higher number means a weaker yen, i.e., it takes more yen to buy a dollar.

It’s hard separate out the impact of two different forces. The first, which we discussed in a previous post, is the growing gap between interest rates in the US and Japan. When US rates are much higher than those in Japan, investors send money from Japan to the US, which pushes the value of the dollar upward and the yen downward (see chart below).

Note: Monthly average except March, which is March 24

The second factor is the impact of Russia’s invasion of Ukraine and uncertainty about where all this is headed. One thing’s for sure. The war is adding to the disruption of supply chains that had begun with COVID. That not only raises inflation but also risks cutting growth in many countries. In past crises, the yen had strengthened as a “safe haven” currency, but in this crisis, investors are fleeing it.

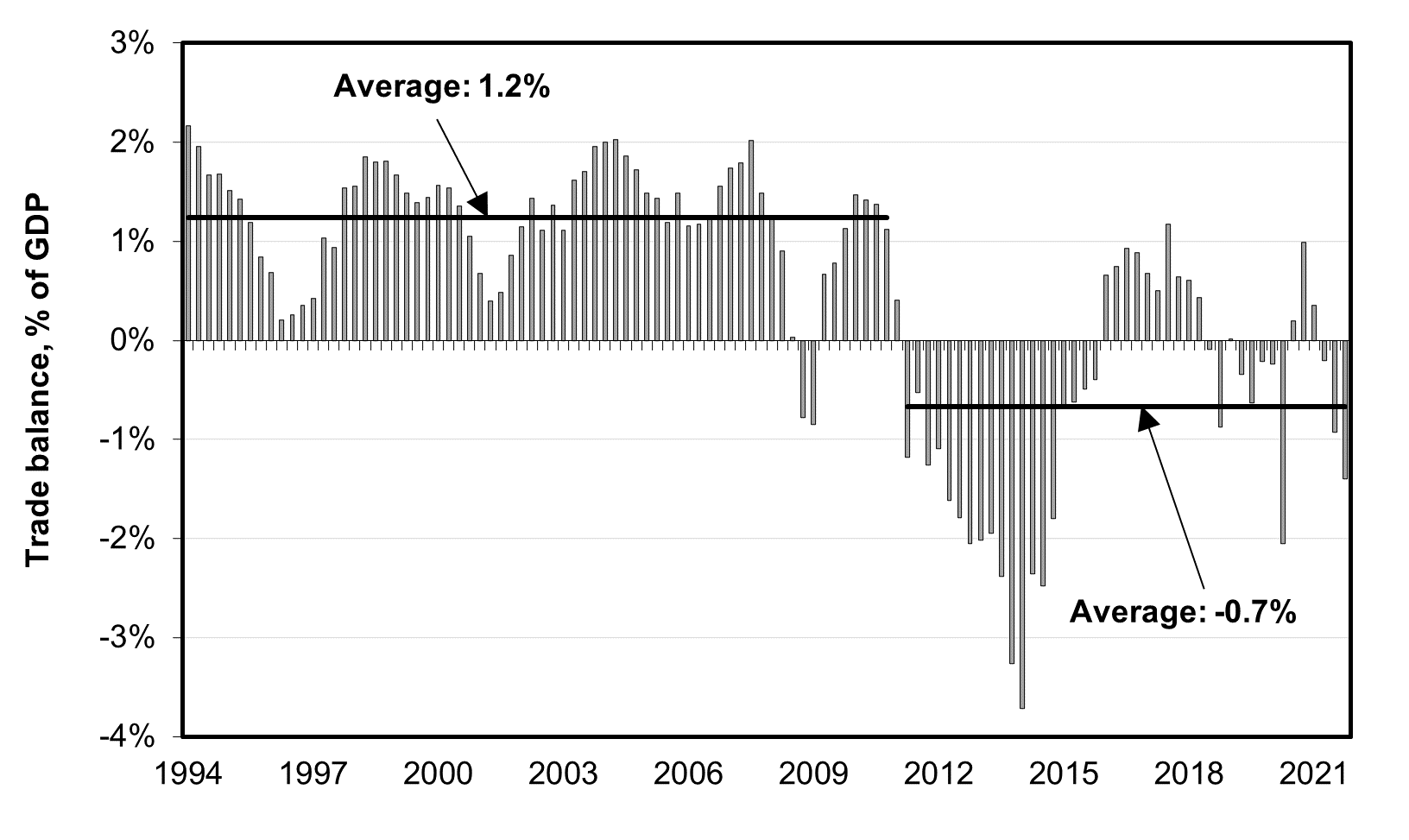

In the background of all this, a country once known for its large trade surpluses now runs a trade deficit more often than not. From 1994 through 2010, Japan’s trade surplus in goods and services averaged 1.2% of nominal GDP per year. From 2011 onward, it has averaged -0.7% (see chart below). All other things being equal, a chronic trade deficit makes a country’s currency weaker than it might otherwise be. The rising price of oil as a result of Russia’s invasion will add to the cost of imports and further expand Japan’s trade deficit.

While Kuroda and some private economists keep saying that a weak yen is a “net positive” for Japan, others close to the BOJ as well as some other private economists disagree. Some of these analysts doubt that Kuroda can maintain this stance if the yen weakens to the so-called “Kuroda line” of ¥125/$. It is called “the Kuroda line” because, back in 2015, Kuroda defended a yen as weak as ¥125 as still a net positive for Japan.

Hideo Kumano, executive chief economist at Dai-Ichi Life Research Institute told Bloomberg, “If the yen reaches the Kuroda line, there’s a risk that the BOJ will suddenly change its stance. The BOJ generally sees a weak yen as good for the economy, but things get very complicated when the weakness comes at the same time as a surge in oil prices.” Over at Mitsubishi UFJ Research & Consulting chief economist Shinichiro Kobayashi commented, “Businesses and households are becoming increasingly aware of the cost of commodity prices and it’s becoming hard for Kuroda to emphasize the benefit of a weak yen.”

Most interesting of all was a comment from Hiroshi Watanabe, who ran the BOJ’s currency policy from 2004-07. Watanabe maintains close contact with his former colleagues, including Kuroda. He told Reuters: “The Bank of Japan continues to say a weak yen is good for the economy. But if crude oil prices keep rising, it's uncertain whether it can keep saying so.” However, he added, even if the BOJ changes its mind and the Kishida administration decided that the downside of a weak yen surpasses its upside, there is little that Tokyo can do.

Still, there is little that policymakers can do to arrest yen declines, he told Reuters. “Intervention [in the currency market to stop yen falls] won't work,” given the huge size of the global currency market. Nor, he said, should the BOJ raise interest rates given the economy’s weakness. “Tightening now would be doing something useless.” What could Japan do then? “For the government, the key is to come up with a strategy that allows Japan to run trade and current account surpluses,” such as by nurturing new businesses, Watanabe said. Even the most strenuous efforts along that line would take years to show an impact.

In the meantime, the restrictions due to COVID, the rising price of oil, and supply line disruption have led a majority of economists to predict that Japan’s GDP will show a decline in the January-March quarter.

For more on how a weak yen hurts Japan, see our previous post below.

I truly enjoy reading your articles on this blog and on the Oriental Economist. I tried reaching you there by sending an email. My name is Dennis Tesolat and I am the general secretary of an Osaka based labour union. We are planning some symposiums for the Autumn and I would love to talk to you about possibly presenting. I can be reached at tesolat@generalunion. thank you.

I private is welcome because my BUISINES is small and in target is Japanese person and peoples only