BOJ Finally Pulls the Trigger on Rate Policy, But It’s a Low-Caliber Gun

How Much Change When BOJ Eventually Tweaks? Part 2

Source: Wall Street Journal

(I will soon publish an update on the Nippon Steel merger situation in the aftermath of President Joe Biden’s statement opposing it.)

The Bank of Japan (BOJ) finally pulled the trigger on tweaking its interest rate policy and here are the key takeaways:

1. The most important takeaway, as I wrote in last week’s post, is that this is more of a change in form than in content. For the most part, the BOJ is changing the mechanism by which it keeps interest rates low. Part of the change of policy concerns overnight interest rates, the basic policy rate used by most central banks. The BOJ has raised this by 0.1% from negative -0.1% to a range from 0.0% to 0.1%. Most BOJ watchers believe it may very gradually raise overnight rates over the next year or so to 0.25% or perhaps 0.5%. Some, however, believe it could raise rates to 2% or more. Nonetheless, in Governor Kazuo Ueda’s press conference following the May 18-19th meeting, he clearly stated that its policy would remain “accommodative,” i.e., it will keep interest rates low. Moreover, in his speech in February, Deputy Governor Shinichi Uchida said real interest rates would remain negative for quite a while, i.e., below the rate of inflation.

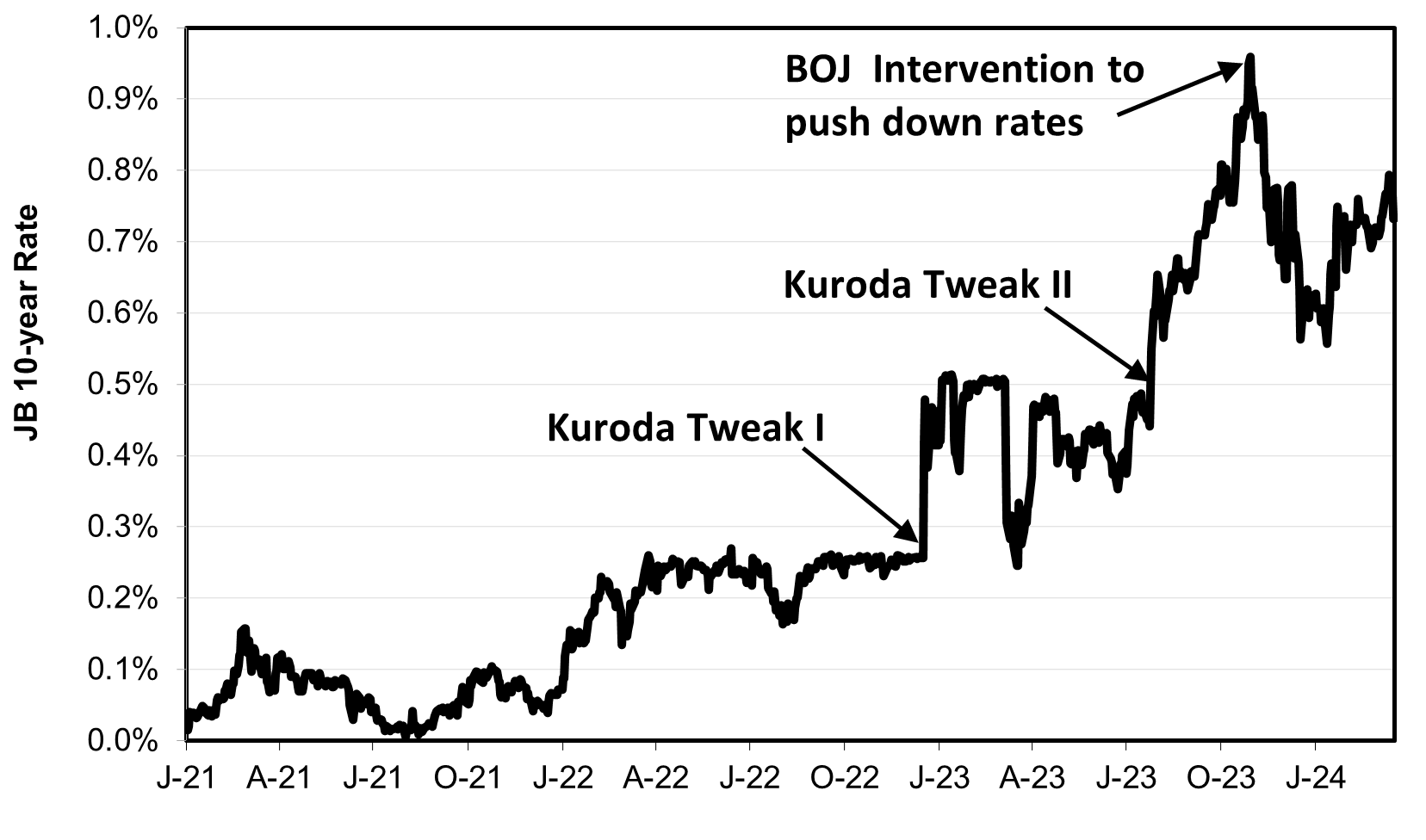

2. The second part of the shift was ending the so-called Yield Curve Control (YCC). That means that the BOJ controls not only overnight rates but also longer-term rates. It has meant that the BOJ would create, and spend, however much money it took to keep rates low, most recently to keep the 10-year Japan Government Bond (JGB) no higher than 1%. Previously, it was kept close to zero, and then at 0.5. While ending the mechanism of YCC, Ueda said the BOJ will continue to buy the same amount of JGBs as it is currently buying in order to keep rates low. How low it has not said; part of ending YCC is ending a specific announced goal for the ten-year interest rate. In any case, it is not clear how much the BOJ will actually have to do in the next year or two to meet its goals. Interest rates for 10-year Japan Government Bonds (JGBs) barely moved after yesterday’s announcement. As of this hour, the yield is only 0.73%. In fact, it is down a tiny bit (0.03%) from the level before the BOJ announcement (see chart at the top). As discussed in my recent post, the lack of big demand for credit in the private will hinder 10-year rates from shooting up.

3. Ueda also made it clear that the Bank still sees inflation too low as the biggest danger, not inflation too high. The BOJ seeks 2% inflation (all prices except fresh food and energy) led by domestic demand. It also believes that this requires nominal wage hikes above 2% and closer to 3%. If ongoing inflation does get too high, Ueda said the BOJ will raise interest rates, but, as of now, it is not absolutely certain that inflation will reach the level the Bank wants. While current headline inflation is too high, the Bank (correctly) feels that most of this is imported inflation due to rising global commodity prices and a weak yen. Moreover, it continues to feel this is a temporary phenomenon, even if it has lasted longer than the BOJ initially expected. The Finance Ministry agrees. So does the International Monetary Fund (IMF), which predicts that headline inflation will fall to 1.9% in 2025 and then 1.6% for the next three years.

4. The trigger for the BOJ moving now, rather than later, was the initial figure of 5.3% nominal wage hikes in the initial spring shunto wage negotiations between the unions and Japan’s biggest companies. That led the Bank to bet that wage hikes for all employees, including the 84% who are not unionized, will reach the desired 2%-plus level. In the next part of this series, I’ll discuss the huge uncertainties in the evidence the BOJ is using to make this judgment and question why it did not wait until June or July to make its move.

5. Contrary to expectations, the yen did not strengthen when the BOJ ended negative interest rates and YCC. On the contrary, it has risen in the past few weeks and, as of this hour, it is at 151.2/$. Moreover, traders now expect the yen the end this year much weaker than they thought just a few months ago. Normally, the yen should strengthen when the gap between American and Japanese interest rates narrow. A change in BOJ policy was expected to narrow that gap. Now the situation is not so clear. Today, however, the yen is about 6 points weaker than it would normally be with today’s interest rate gap (see chart below). The yen spends two-thirds of its time about 4 points above and below the forecast rate. I’ll discuss the reasons for the yen’s weakness in a future post.

Source: Actual yen from Wall Street Journal; forecast by author