China’s BYD Aiming to Seize Toyota’s Crown Via BEVs

Smugness is Achilles' Heel of Japanese Automakers

Source: https://cleantechnica.com/2025/01/31/byd-becomes-4th-best-selling-automaker-in-the-world/; https://cleantechnica.com/2024/09/12/byd-closer-to-becoming-1-automaker-in-world-than-i-thought/#google_vignette; and press reports Note: Since foreign companies (except Tesla) all have to operate with 50:50 joint ventures in China, the global sales figures include just half of JV sales in China.

Seeming to come out of nowhere just a few years ago, Chinese automaker BYD is positioning itself to challenge Toyota for its crown as the world’s top automaker. Last year, it leapfrogged past Hyundai, Ford, Honda, Nissan, and Suzuki last year, to become the world’s fifth-largest automaker. This year’s sales will be around half of Toyota’s, up from a mere 7% in 2021. It wants to sell 6.5 million in 2026 (1.5 million of them in overseas markets). If it succeeds, it will likely outdistance GM and Stellantis this year or next to rank third (see chart at the top). What makes all this even more remarkable is that it only sells BEVs (battery-operated vehicles) and PHEVs (plug-in EVs). No gasoline vehicles. No conventional hybrids (HEVs).

Now it’s moving to challenge the leaders in their own strongholds. By 2030, it plans to sell half its vehicles outside of China, i.e., about five million out of 10 million or so. The company has already established plants in Thailand and Brazil, with plans for additional facilities in Hungary and Mexico. While Donald Trump’s trade war will hurt Toyota, Stellantis, and GM, BYD will be okay since it has little presence in the US.

BYD is not alone. Its compatriot, Geely (including its foreign subsidiaries like Volvo), has also surpassed all the Japanese companies except Toyota and now ranks eighth (see top chart again). 40% of its sales are BEVs and PHEVs. 36% of its sales are outside of China. If Geely reaches its sales goal of 5 million by 2027, it will surpass Ford and perhaps even Hyundai.

Japan’s Falling Stars

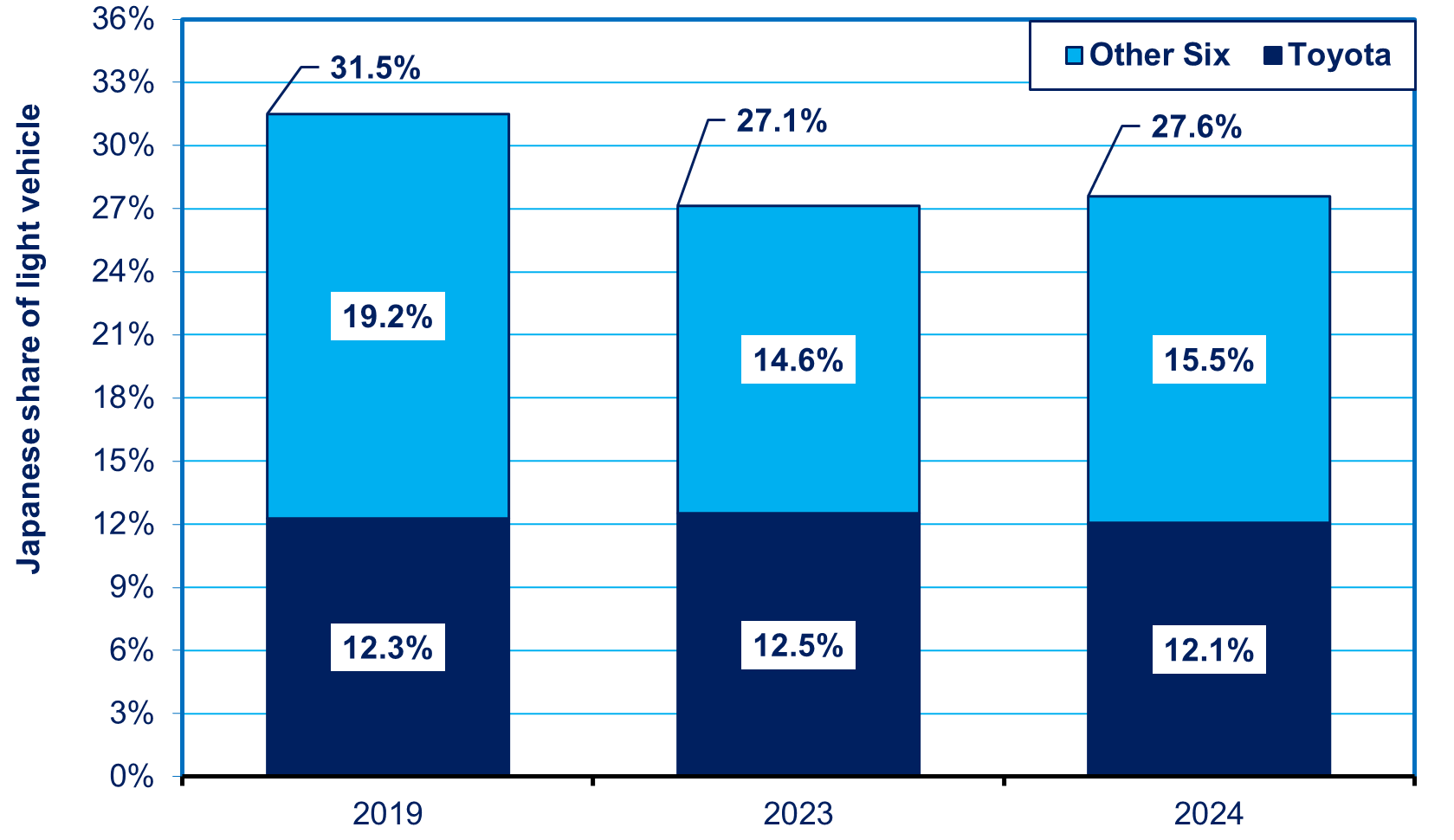

While the stars of BYD and Geely are rising, those of Japan’s companies are falling. Japan’s global market share peaked in 2019 at 31.5%, with most autos produced overseas. That’s an unbelievably impressive number. However, as of 2024, it had declined by four percentage points to just 27.6% (see chart below). Mitsubishi, Subaru, and Mazda now sell less than Tesla.

Source: https://www.oica.net/production-statistics/ and press reports Note: The other six are Honda, Nissan, Suzuki, Subaru, Mazda, and Mitsubishi.

In China, the world’s biggest auto market, Japanese sales have fallen for three years in a row. Japanese companies can’t supply the BEVs and PHEVs that each comprise a quarter of all auto sales. Mitsubishi simply abandoned China in 2023. At both Honda and Nissan, sales halved from 2021 to 2024. Since a third of their sales was in China, that was a big hit. Toyota’s share fell “only” 8% but market growth was so rapid that Toyota’s slice of the China market nosedived from 9% to 5.6%. What a missed opportunity.

It's not just China. In the first quarter of 2025, Honda’s sales outside of Japan and China fell 4% while everyone else’s sales in those markets grew 5%.

Nissan announced in late May that it would cut its global capacity further, from 3.5 million vehicles today to just 2.5 million. That’s less than half of the six million it sold in 2017. Nissan may not survive as an independent company. It tried to sell itself to Honda but then demanded an equal partnership. The deal collapsed.

While Toyota has so far maintained its share, I’ll detail below and in Part 2 why it’s vulnerable.

Detroit Redux

Japanese automakers are losing customers because they suffer from the same smugness that blinded Detroit to the Japanese challenge in the 1970s. Just as Detroit dismissed the shift to more gas-efficient and lower-defect cars back then, Toyota, Honda, et. al. deceive themselves about BEVs. The International Energy Agency (IEA) currently forecasts that BEVs will comprise a third of all vehicle sales by 2030 and 45% by 2035. S&P made a similar forecast last year. Despite Trump’s efforts, JD Power says BEVs will rise from 9% of the American auto market this year to 26% by 2030. An S&P report headlined the point: “Slower EV Growth Offers Temporary Relief To Legacy Automakers [emphasis added].”

The problem is that Japanese companies see hybrids as a panacea. So they are failing to supply the kind of vehicles to which customers are shifting at a surprisingly rapid pace.

Global sales of gasoline-only Internal Combustion Engine (ICE) vehicles peaked in 2017 at 83 million and, by 2024, had plunged to just 60 million. Their market share has fallen off a cliff to a mere 67% last year. By 2030, ICEs could be only 20 to 25 million, according to S&P. What a fall from grace in just a dozen years.

Conversely, BEV sales rose from a negligible amount in 2017 to 16% of the global market in the first quarter of this year. PHEVs account for another 6% while hybrids comprise 14.4%. For 2025 as a whole, the BEV share could be as high as 18%, given that the IEA sees the combined share of BEVs and PHEVs at 25% this year (see chart below).

Source: https://www.bloomberg.com/news/articles/2024-01-30/world-hit-peak-gas-powered-vehicles-as-evs-gain-market-share; press reports

Currently, in the major markets that PWC covers—85% of the entire global market—BEVs and HEVs each account for 16% of the auto market, the HEV share making Toyota et. al. think they’ve judged the market correctly. However, says PWC, by 2030, customers in these markets will buy 30% more BEVs than HEVs and twice as many as PHEVs.

Overcoming Three Obstacles

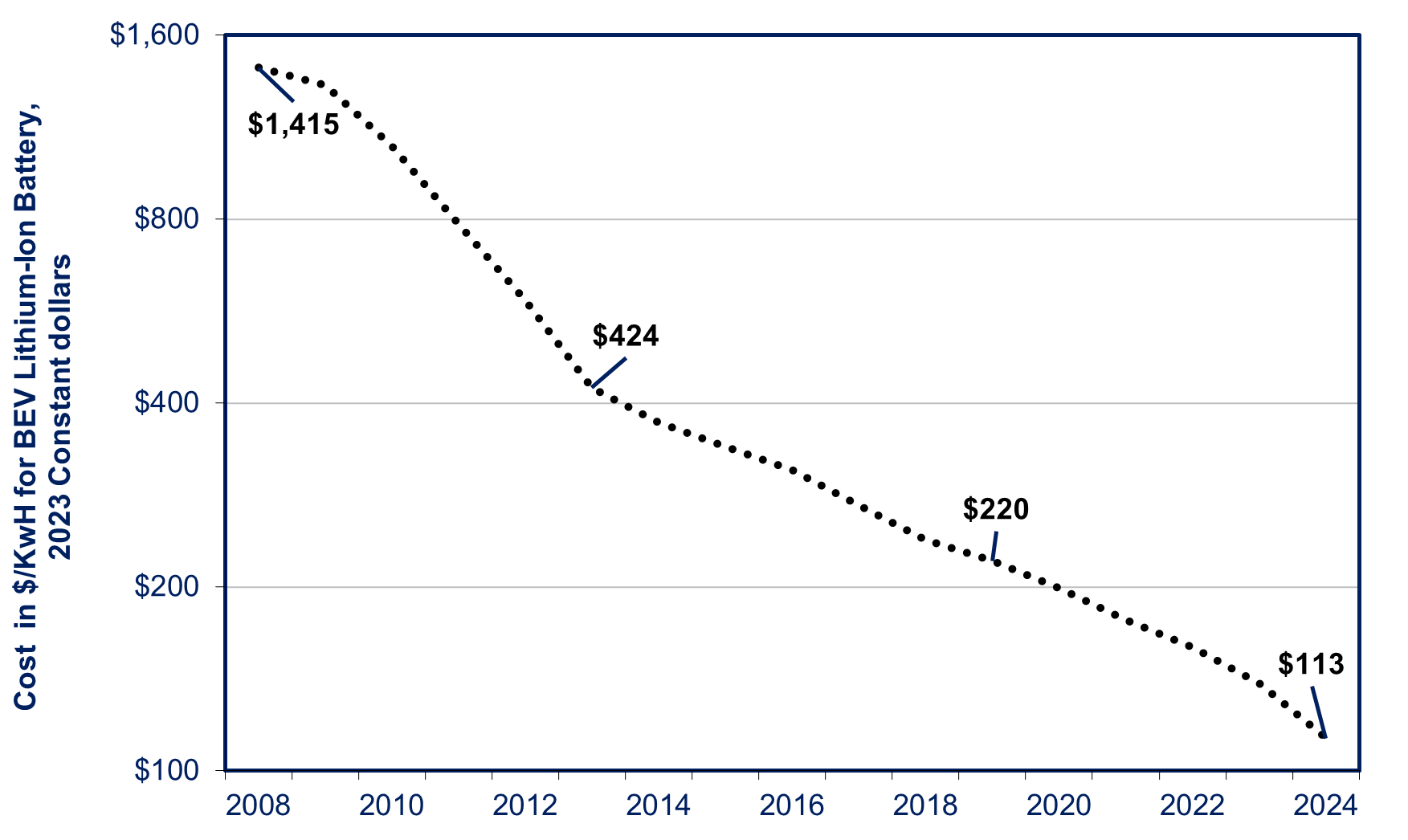

To transform BEVs from a luxury item to a product for the masses, three obstacles must be overcome. The first is high prices. Batteries comprise 40% of a BEV’s production cost, and technology is bringing down those costs at a rapid rate (see chart below). Gartner says advanced manufacturing methods are reducing production costs even faster than battery improvements.

Source: https://www.energy.gov/sites/default/files/2024-08/FOTW_1354_web.xlsx; https://about.bnef.com/insights/commodities/lithium-ion-battery-pack-prices-see-largest-drop-since-2017-falling-to-115-per-kilowatt-hour-bloombergnef/ Note: This is shown on a logarithmic scale, so every halving of the price has the same vertical height.

In addition, automakers are bringing out more affordable models. Back in 2018, you had to hand over $100,000 for the cheapest BEV with a 300-mile range. Now you can buy one for less than $50,000 before subsidies. Stellantis now offers an SUV in Europe that costs exactly the same ($31,000) whether you get a “mild hybrid ICE” version or a BEV.

The price difference between an ICE and a BEV in the US was 50% in 2021, but only 12% by December 2024. In Europe, the price gap tumbled 53% in 2018 to 22% last year. It’s a matter of time before BEVs become cheaper to buy than ICEs, even without subsidies. In China, the prices are already equal.

The second obstacle is range anxiety, which is a matter of technology, e.g., a shift to solid-state batteries, and installing more chargers. The third is how long it takes to charge a car. BYD claims its improvements in technology allow a charge to 80% full capacity in 30 minutes. When solid-state batteries become practical, that will be a game-changer.

Blind Spot

To virtually ignore models that will account for almost one out of every five vehicles this year—and perhaps one of three in five years—seems rather foolhardy. Nonetheless, the Japanese automakers currently produce only about 2% of the global output of BEVs. They’re biased against BEVs, and produce few PHEVs, because they see them as a threat to their investments in conventional hybrids (HEVs). That’s particularly true of Toyota, whose HEVs comprise almost half of their global sales, most of the rest being ICEs. At Honda, it’s 80% ICEs, 20% HEVs, and a trivial number of BEVs. No wonder Honda’s global market share fell by a quarter, from 6.1% in 2019 to just 4.6% in 2024.

It's undeniable that Toyota’s HEV-focused strategy is earning it lots of sales and profits at present. However, today's profits come at the expense of its ability to produce high profits in 2030 and beyond. For one thing, if S&P is right, sales of HEVs and PHEVs will peak around 2028 as BEVs increasingly dominate.

While the Japanese players are producing more BEVs, they’re doing so at a snail’s pace. Of the top 23 BEV producers in the world in 2024, Honda came in 23rd at a piddlkng 40,000 autos, and Toyota was 20th at 140,000. By contrast, VW sold nearly 750,000; BMW 425,000; Hyundai 400,000, and so forth (see chart below).

Source: https://evboosters.com/ev-charging-news/top-20-bev-sales-2024-byd-the-new-king-of-full-electric-cars-in-2025/ and press reports Note: Japanese companies in bar with angled lines; legacy non-Chinese companies in dark blue bars

Worse yet, Japanese automakets have dratsically cut their five-year BEV targets. Honda lowered its 2030 goal from 30% of its total output to 20%. Who knows if they’ll even make that? Toyota still denies press reports that it lowered its goals of1.5 million BEVs in 2026 and 3.5 million in 2030, or 30% of sales. However, given that it reportedly plans only 1 million as late as 2027, its purported goal for 2030 seems rather far-fetched.

Toyota et. al. may think they can rev up production and put out a competitive product whenever they want to, but that’s easier said than done. Companies improve their production and marketing competitiveness via the “learning curve,” i.e., learning by doing. Failure to produce BEVs while others are doing so means falling behind, even for technological powerhouses. SONY and others found that out, they tried, and failed, to put out a competitive PC. Automakers who wait too long may find it harder to catch up (more on this in Part 2).

The more Trump hinders BEV production in the US, the more he’ll deprive US producers of the required learning curve benefits. He’s “Making China Great Again.”

The slowdown in the pace of BEV growth has led many companies to scale back their BEV goals. Yet, none seem as antagonistic as Toyota, none so aggressive in trying to slow others’ efforts. Perhaps that’s because it has the most to lose if it fails to recoup its enormous investments in hybrids. The New York Times revealed that, in the US, Toyota financed candidates opposed to BEVs and initially cheered Trump’s victory due to his anti-BEV stance. This year, it even aided the Republicans in Congress who violated longstanding Congressional rules in order to prevent California from doing what it has done for decades: enforcing its own stricter standards for cars sold there. The motive was to lessen demand for BEVs. California mandates zero emissions by 2035. Sixteen follow California’s rules, and the entire group accounts for 40% of the US car market. That gives automakers a big incentive to provide the BEVs these states demand. The issue is now going to court. By contrast, a few years back, Honda, along with BMW, Ford, Stellantis, Volkswagen, and Volvo (owned by Geely) signed a “California Framework” agreement with the state to abide by its standards, regardless of what happens at the Federal level. So far, I’ve found no response by these companies’ response to the latest developments. It’s unclear what any of the automakers will do in the midst of this uncertainty. Meanwhile, BYD and Geely will move ahead to become even more competitive in BEVs all around the globe.

Coming in Part II: Toyota thinks it called the market right with its focus on HEVs; what will that decision look like in 2030?

To receive new posts and support my work, consider becoming a free or paid subscriber.

To provide more support, donate several subs at $50 each. You do not need to name the sub recipients, just how many. This is a one-time contribution; it does not repeat automatically. Please click the button below.

I think this will be an interesting test, but I am unconvinced that BEVs are the threat you think they are outside China and inside China they are selling as much as they are because of subsidies. My bet is that Toyota's HEVs are the customer desired answer and the only reason for EV growth are government policies that make them more attractive than they actually are

You mention issues with EVs - price, range/charging time - and claim that they are being resolved, which they probably are. You omitted two others - resale value and weight.

Weight is probably impossible to solve assuming you want EVs to have decent range because batteries are just heavier than a tank of fuel. Also battery charging time is IMO only partly solved. It is solved for the second car in a two+ car household because the second car typically just does a short range commute most days and therefore can be charged overnight, but the primary car is generally expected to do more - tow things, drive to distant vacation spots etc. that will require it to stop and charge somewhere. 30 minutes sounds OK until you compare it to a non-EV that can be refueled in 5 minutes. I know the argument is that you spend the 30 minutes having a coffee/meal, going to the toilet and so on but that only partly solves the problem AND it only works when there are 6 times as many charging spaces as there are fuel pumps because only one car can be charged by a specific charger at a time and it takes 6x as long

Resale value depends heavily on the range of the EV not declining precipitously as it ages and my understanding is that this is not a solved problem in the newer battery technologies. Sure you can (in theory) replace the batteries but given that the battery is 40% of the cost of the car that means that the resale value in a few years will drop fast because of the need to replace the battery and still have the car cost less than a new one. The jury is out on whether BYD and Geely cars will still be running in 5-10 years, but I can buy a Toyota and be confident that it'll run for well over a decade assuming no major incidents. Even if I plan to sell the car on in five years, I get a higher price for it because the next buyer is confident that the car will still run. Moreover, until EV chargers are available widely in poor places, the market for second hand EVs will be smaller (and hence prices will be lower). The final destination for old cars in first world nations is often third world nations and I find it hard to believe that EVs will be running in Africa in the next decade. I rather doubt they'll be running in the less developed parts of Asia either (the stans or, say, Laos)

I have a further challenge. What kind of car do you personally drive? and what do you plan on buying next? Ask enough people around the world those questions and you'll get a feel for whether EVs are actually going to take off. My strong intuition is that people will prefer not to buy EVs

Pure EVs have other problems, like poor cold weather performance, that reduce

Transition into EV will mean the millions of jobs in Japan, but Trump tariffs have already done that anyway. Now, Toyota has a motivation to go into EVs, but it refuses to do so as it wants to save the suppliers. Toyota's acquisition of Toyota Industries is a very controversial move that makes my point exactly. Even if Toyota wants to move into EVs completely, it will fail to secure the critical resources and supply chains as China has totally dominated everything to wage a price war for decades.