China’s Growth Prospects, Part I

Japanification, Slow Decline, or Renewed Boom

Source: https://www.imf.org/en/Publications/WEO/weo-database/2023/April/download-entire-database

Note: PPP = Purchasing Power Parity (in constant 2017 $) to adjust for changes in price levels and currency rates among countries

What’s in store for China?

Will China, like Japan before it, suffer a property and financial crash that triggers a couple of lost decades? Other countries have also suffered such crashes, without suffering lost decades, including the US in 2008-09. What was different about Japan, and now China, is that the crash occurred in an economy corroded by structural flaws, from suppressed household income and thus consumer demand, poor productivity growth, and protection of zombie companies to the poor management of the mountain of bad debt. Consequently, Japan’s per capita growth abruptly fell off a cliff from nearly 4% during 1975-90 to just 0.7% during 1991-2022. China is vulnerable if it suffers a similar financial crash. Daniel Rosen, co-founder of the Rhodium Group argues that a ratchet down to 3% growth for the rest of this decade is the “best” it can do, even if it undertakes serious reform. Without such reform, growth would be worse.

Suppose, however, that China avoids a crash. In that case, China, like Korea before it, may simply see a continuation of the gradual deceleration it has already been experiencing. In this scenario, China’s growth would decelerate to a 3-4% pace in the next few years and then deteriorate further. Bloomberg Economics just lowered its forecast and says that growth in total GDP (not per capita) will steadily slow to less than 1% by 2050 (see chart below). This, as will be detailed below, is the mainstream view.

Note: Bloomberg GDP forecast converted to per capita GDP using population projections

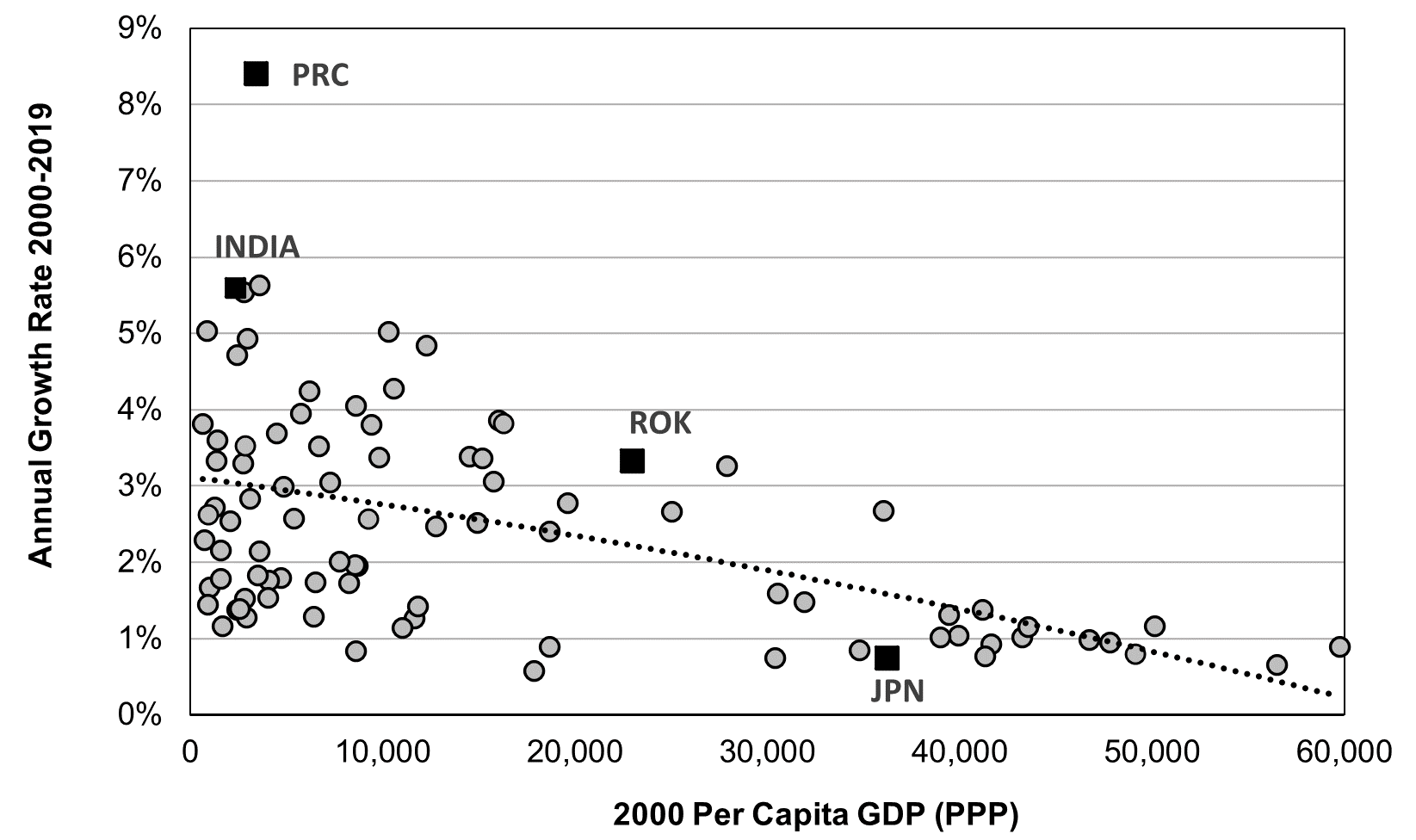

Some of the slowdown in China’s growth is occurring because in all countries growth slows as they become more affluent. This is due to the law of diminishing returns, as I’ll explain below. Unfortunately, Beijing, like Japan before it, has worsened this natural slowdown by resorting to politically/ideologically motivated and economically incompetent economic strategies. In China, these include: reviving the dominance of state-owned enterprises that have lower productivity than private firms; increasing the role of Communist Party commissars at the private companies; suppressing the rise of household income and consumption needed by a maturing economy; and, maintaining demand, relying instead relying on excess investment in housing and infrastructure and building up problematic private debt in the process. Already, China’s growth rate has fallen below Korea’s when we compare both at the same level of real per capita GDP (see chart at the top).

Worse yet, it’s very hard to achieve a smooth deceleration like Korea’s. Usually, as documented in a widely-cited 2013 paper by Lawrence Summers and a co-author, rapidly growing countries see an abrupt and turbulent downshift in growth by a few percentage points. Such drops are typically provoked by an internal or external shock, as happened to Japan in the the wake of the 1973-74 oil shock. By contrast, Korea and other resilient Asian “tigers” bounced back from the calamitous financial crisis of 1998-99. The downturns are usually even more severe in authoritarian countries, with China being the prime example discussed in this paper. It’s not just Beijing’s ideological economics. Xi has added a capriciousness typical of authoritarians, as evidenced by his COVID lockdown and its helter-skelter lifting without sufficient vaccinations. Adam Posen discussed this factor in a recent Foreign Affairs essay.

While Japan was certainly not an authoritarian state, it was a one-party democracy and most one-party states have difficulty making course corrections. Korea, by contrast, moved past the era of military dictatorship and then the one-party state during the 1998-99 Asian financial crisis, and this yielded some policy breakthroughs that helped it avoid pitfalls.

There is a third scenario: a return to the boom times. Beijing claims that the West exaggerating China’s troubles and it can achieve “average annual growth rate of at least 8% until 2035 . . . {and] 6% from 2036 through 2050.” It will do this because a statist China it is still catching up to the West and because it will capture the commanding heights of critical technologies and products via efforts like its state-led “Made in China 2025” program. This is a chimera. In the West, Nicholas Lardy argues that a return to market-oriented policies would enable China to grow 6% to 7% per year for the next decade; if it does not do so, its growth will languish at 3-4% per year for the next four to five years. If either Beijing’s pipedream or Lardy’s argument (to be discussed in a follow-up post) were to come true, China would soar as no other economy has even come close. By 2035, China would be twice as large as the US in total GDP (and reach half its per capita GDP). I don’t think that’s in the cards, with or without reform.

Mainstream View Sees 4% Growth For Next Few Years

Very few experts outside of China believe China can return even to 6% growth, let alone 8%. The mainstream view is that China will grow 4.7% this year, and about 4% next year. That’s just a 0.5 percentage points cut from estimates a few months back and they already take into account China’s myriad problems. Moreover, the International Monetary Fund projects that, from now through 2028, per capita growth will average 4%, and slowly drop to 3.7% by 2028. Just three years ago, the IMF was forecasting 5.6% for the following four years. Again, this 2 percentage point shift takes into account the mounting financial stresses.

These projections, however, presume that China does not suffer a huge financial shock because Beijing has the instruments to avoid it, even at the cost of further eroding the economy’s underlying fundamentals. The latter is what Japan did for so long with its handling of the bad bank debt. The most pessimistic believe China can no longer avoid such a crash for long, but many of the latter have been saying that for years.

No one really knows whether the mainstream or the pessimists are right. While economists are good at pointing out bubbles, they’re incapable of forecasting even whether—let alone when, and how badly—such a bubble may pop. There are simply too many inherently unpredictable factors involving human behavior. Lots of economists warned of the American housing/financial derivatives bubble in the 2000s. However, virtually none, other than those who are always crying wolf, predicted a catastrophe as severe as the world saw in 2008-09. Moreover, If China does suffer such a shock, rather than staving it off, no one can reliably tell us how well or badly the Xi regime will handle it.

One other issue for the experts to ponder: Is China more of an economic and political problem for the world when it is too strong or when it is too weak?

4% Per Capita Growth Would Be Terrific—If China Can Achieve That

Many people see “only 4%” per capita growth as “bad,” but that’s actually higher than virtually any other country at the same level of per capita GDP. So, that’s probably the best China can do. Xi’s stubborn refusal to recognize China’s flaws as flaws suggests that even 4% is not guaranteed.

A country’s per capita GDP is one of the main factors determining how fast countries can grow over the medium term. Poor countries grow slowly. As they industrialize, the speed picks up and a few, like Japan, Korea, China, India, Vietnam, and Bangladesh, do so at quite high levels. By investing a lot in the most modern machinery in both farming and manufacturing, industrializing countries raise output per worker by leaps and bounds. At the same time, workers move from the farm to the city where their productivity is much higher. Roads, electricity lines, etc. all raise productivity even more. Eventually, however, that process runs into diminishing returns and growth slows.

By this standard, China’s per capita growth during 2000-2019 was spectacular: 8.4% a year, especially since it came on top of 8.5% during 1980-2000 (see chart below). No other country has grown so fast for 40 years. Japan came close. Its “economic miracle,” lasted 23 years (1950-1973), and per capita GDP grew 7.7% per year. Korea came even closer: 7.5% over 37 years (1960-1997).

Note: Only includes countries with at least 5 million people and per capita growth of at least 0.5% per year, and excludes major oil exporters

China’s unrivaled performance resulted from three factors:

1) A very low base, just $700 way back in 1980 and still just $3,400 as of 2000, just about the same as Japan’s per capita GDP at the start of its economic miracle, Korea’s level was $1,390 in 1960;

2) Very wise and competently executed policies during much of this period; and

3) A benign world environment eager at that time to aid China’s export-led growth and to take advantage of its welcome mat for foreign multinationals that brought in new technologies.

Once China moved from extreme poverty to upper-middle-income status, its growth decelerated as it does in every country. Still, as the chart below illustrates, 4% growth is higher than in almost any other country at China’s level of development.

Note: The growth rate is based on the IMF’s forecast of real per capita GDP in 2024 and of growth during the 2024-2028 period

The fact is that China’s growth has been steadily slowing since 2006 and, for the reasons given above, there is nothing either surprising or worrisome in such a slowdown by itself (see chart below).

Source: IMF (see above) and World Bank at https://databank.worldbank.org/source/world-development-indicators

Note: Figure for 2023 is an IMF estimate and 2024-2028 are IMF forecasts

China’s real problem is that, beginning under President Hu Jintao (2003-2013) and now very forcefully under Xi since 2013, Beijing retreated from the policies that had lifted hundreds of millions from poverty. So, the country’s growth slowed more than it needed to. In fact, as noted above, ever since 2008-2010, when China reached around $10,000 real per capita GDP, it has been growing more slowly than Korea did when it had reached the $10,000 level (see chart at the top of this post).

Indeed, for most of the past decade, China has fallen closer to Japan’s pre-lost decades trajectory than to Korea’s. If China really does begin to look anything like post-1991 Japan, it will do so when its living standard is only a bit more than half of Japan’s level in 1991. Hundreds of millions of people will be left far below middle-class standards (see chart below).

Note: IMF forecast for 2023-28 for China

Blinding Oneself To Consequences

Poor economic performance limits not only China’s geopolitical ambitions; it also risks social dislocation at home. After reporting that unemployment among adults in their 20s had reached 20%, almost double the level in 2018, Beijing announced it would no longer release the data. Having lots of young men too poor to get married has been a recipe for unrest in many a country. And yet, like authoritarians (and others) elsewhere, Xi seeks to hide from himself the consequences of his wrongful path.

When the SARS epidemic broke out in 2002, the CCP under President Jiang Zemin suppressed the information, worsening the health crisis. Soon after coming to power, new President Hu Jintao found he still couldn’t get the information he needed from local officials. So—I was told by a reporter at a Chinese business magazine—he loosened press controls and encouraged the press to find the information for him and report it. Not long afterward, Hu revealed that the Party had lied, due to external and internal pressure. Xi, like Jiang, is trying to cure the patient’s fever by hiding the thermometer.

In a follow-up post, I’ll look at Xi’s wrongheaded economics and assess the Japanification analogies.

Richard,

You state that:

"In the West, Nicholas Lardy argues that a return to market-oriented policies would enable China to grow 6% to 7% per year for the next decade; if it does not do so, its growth will languish at 3-4% per year for the next four to five years"

In Nicholas' article he states:

"China’s private sector, which led the rapid growth of the domestic economy during the past 30 years, has lost its power due to political regulations by Chinese authorities...private sector investments have steadily decreased as a result of Chinese President Xi Jinping consistently strengthening regulations while espousing qualitative development rather than economic growth...private sector investments “rapidly weakened starting with the beginning of last year"".

At no point does Nicholas actually explain what the regulations are/were, or how significant (quantity) and prolonged (duration) the decrease in private sector investments were. Nicholas also does not explain what specific "market-oriented policies" are required. Why not? These arguments are not properly explained or substantiated. Additionally, talk is made of "negative conditions", which later are revealed to include a 75% increase in Chinese companies sanctioned by the US, and restrictions on exporting cutting-edge technologies to China (which ironically is driving China to develop more of its own - see recent news re: the new Kirin 9000s chip in Huawei's Mate 60 Pro for example). Despite this, China is expected to grow c. 3-4% for the new four to five years. We should ask ourselves - how much of China's slower growth is attributable to Chinese government regulation, and how much to Western attempts to retard it?

I understand that the West would like China to be more of an economy and government in its own image (and therefore more open to Western corporate interests). In the West, we live in a society where private capital has significant influence both on the economy and on government. In China it's very much the opposite. Understandably, many of us are uncomfortable with this. However, as the phrase "qualitative development" hints at (which means growth that enhances the quality of life, not just economic growth for its own sake), China is concerned about quality of development, including wealth inequality. This is why, for instance, we have seen Chinese government regulation banning for-profit tutoring firms. From a capitalist standpoint, this intrusion on private financial interests is understandably alarming. I know this is an economic newsletter and as such financial interests will prevail in the discourse, but from a social equality and equality of opportunity perspective, I believe there is much to commend it.

Rick, I assume you have chatted directly with Nick Lardy, if not see his PIIE piece that came out this past week. Note Nick had an office just across from Hugh at Yale when I was a grad student, I’d often chat with him while waiting to see Hugh [Patrick].

I have an Chinese 2023Q2 automotive update just out on SeekingAlpha, the link is here but I’ll email a pdf. Key takeaway for you: this year car sales will likely remain close to but below the 2017 peak. Now the average car is much more expensive than in 2017, but employment in the industry is likely falling.

https://seekingalpha.com/article/4632760-china-2023-q2-nev-update-focus-on-guangzhou-automobile