GDP Disappoints in Fourth Quarter

Up Less Than 4% From 15 Years Ago

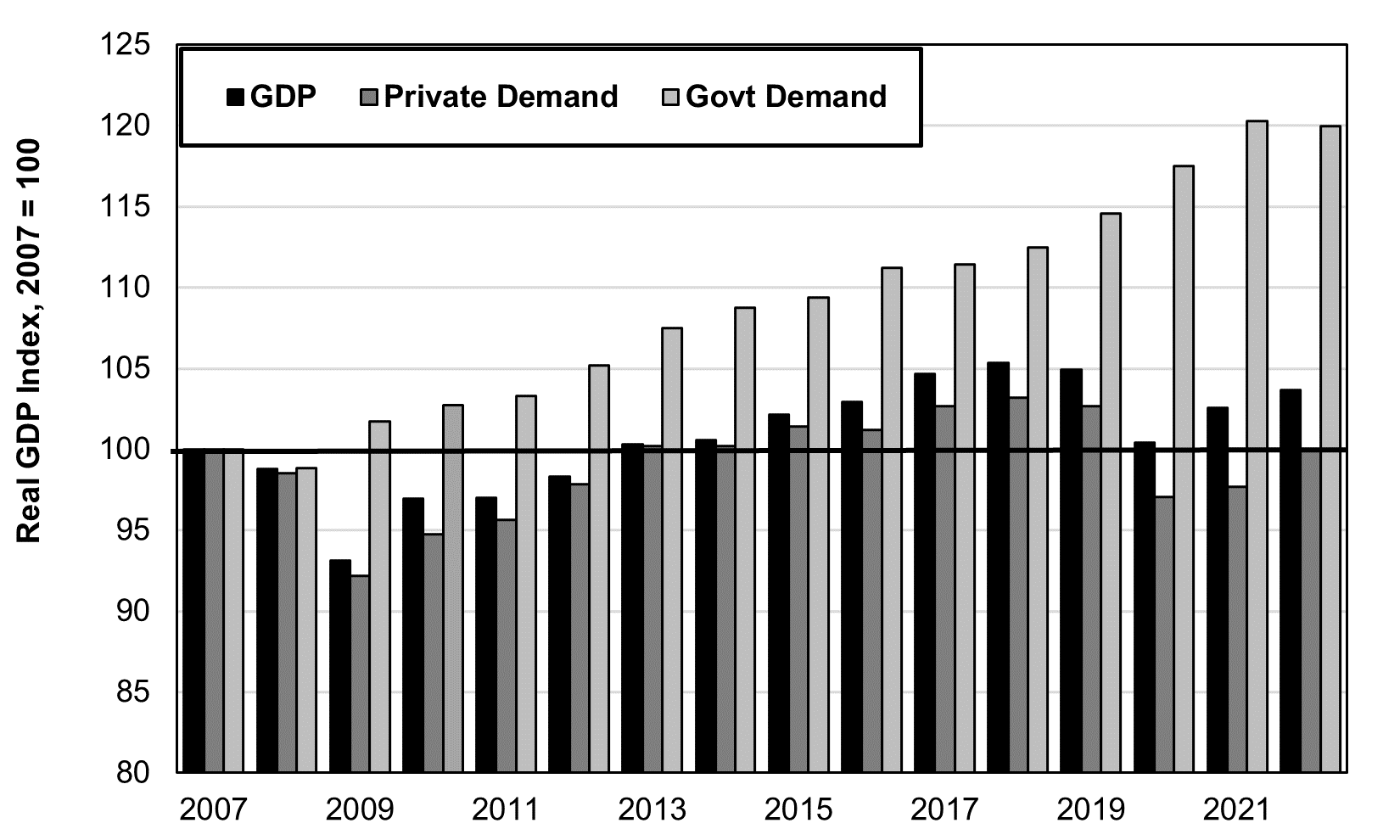

Source: Cabinet Office at https://www.esri.cao.go.jp/en/sna/data/sokuhou/files/2022/qe224/gdemenuea.html

Japan’s GDP disappointed in the fourth quarter of 2022, growing at a meager 0.6% annual rate. Economists had predicted a 2% rebound following the 1% annualized drop in the previous quarter. As a result, GDP is still below the level it first reached five years ago in 2017. That was before Japan was hit by the double whammy of a hike in the consumption tax in October 2019 and then Covid (see chart above).

This puts into question the IMF’s forecast that, in 2023, Japan will show the highest GDP growth among the big Group of Seven countries.

There’s one caveat here. This is a preliminary report, issued before the government has gotten full information on business investment in October-December. When a final report is issued in a few weeks, the number could be revised upward or downward.

Very Slow Growth In Past 15 Years

Regardless of the quarterly ups and downs, what remains clear is that Japan has shown incredibly meager growth in the 15 years since 2007 as seen in the chart below. The lost decades have not ended—at least not yet.

Note: The big GDP decline in 2008-09 was due to the global financial catastrophe

Real GDP is up only 4% from 2007, an annual growth rate of only 0.2%. Private domestic demand—personal consumption, business investment, and housing construction—is back down to the level first reached in 2007. By contrast, government spending is up 20% and has provided almost all of the GDP growth. It is the weakness of private demand that has compelled Prime Minister after Prime Minister, including the current one, to lift spending.

The outright zero growth in private demand is due to a 25% decline in housing construction. That’s not a surprising development in a country where the population is both shrinking and aging. This may surprise those gazing at all the construction cranes building splendid apartments in metropolitan Tokyo, but it’s not surprising to those who see the countryside littered with about 4 million abandoned homes.

However, housing is not the whole story. If the main components of private demand—personal consumption and corporate investment—were healthy, total private demand would be a lot bigger today. However, growth in these two categories has been anemic. Personal consumption is up only 1% compared to 2007, while business investment is up only 2% (see chart below).

Why is personal consumption so stagnant? Mainly because personal income is stagnant. Total real compensation for all employees combined showed a temporary burst in the Abe era as more women and elderly entered part-time and temporary work, but it has now fallen back. It’s now just 3% above its level 15 years ago (see chart below). At the same time, interest income from banks and insurance annuities is down due to the Bank of Japan’s near-zero interest rate policy. To top it off, government social security per senior is down 20% from 1996 and governments have repeatedly raised the consumption tax. How can policymakers expect households to spend more if they leave them with less to spend?

As for the stagnancy of corporate investment, why would companies invest in expansion, or even modernization of equipment, if consumer demand is so stagnant? Growth in exports can only offset this drag on investment to some degree.

It Ain’t Just Population Decline

Perhaps, some might wonder, the numbers look so bad because Japan’s population is declining. Let’s take a look. The population peaked in 2010 at 128.1 million. By 2022, it had fallen by 3%. So, demographics makes some difference, but not all that much. GDP is up 3.7% compared to 2007. Per capita GDP is up 6.8%. So, GDP increased at a dismal rate of 0.2% per year and per capita GDP at a slightly less dismal rate of 0.4% per year (see chart below).

Regarding the effect of population decline on GDP, should one look more deeply at the changes in composition of the population rather than just at the total population size?

For example, the total population size may not have changed much over 15 years, but it has aged greatly, and older people are likely to spend less and less (apart from on healthcare)?

Also, is the demographic *outlook* not a reason for people to be trying to spend less and save more, knowing how difficult future years will be as the working population collapses?

One could say that the future-looking demographic forecasts are as big a factor influencing current spending patterns as the past demographic changes?

Lastly, when looking at populatiojn size in Japan, do you include foreigners who are living, and often working, in Japan? I expect those numbers will be increasing to offset the falling working population, and will be an increasingly large economic factor, even if they only have temporary residency status.

It's not just the economy. In fact, profits are eroding (much) quicker than the economy.

https://mtaylor.substack.com/p/japans-evaporating-profits