Opposition Fumbles Politics Of Consumer Tax Cuts

Ishiba Cries Wolf (i.e., Greece) on Government Debt

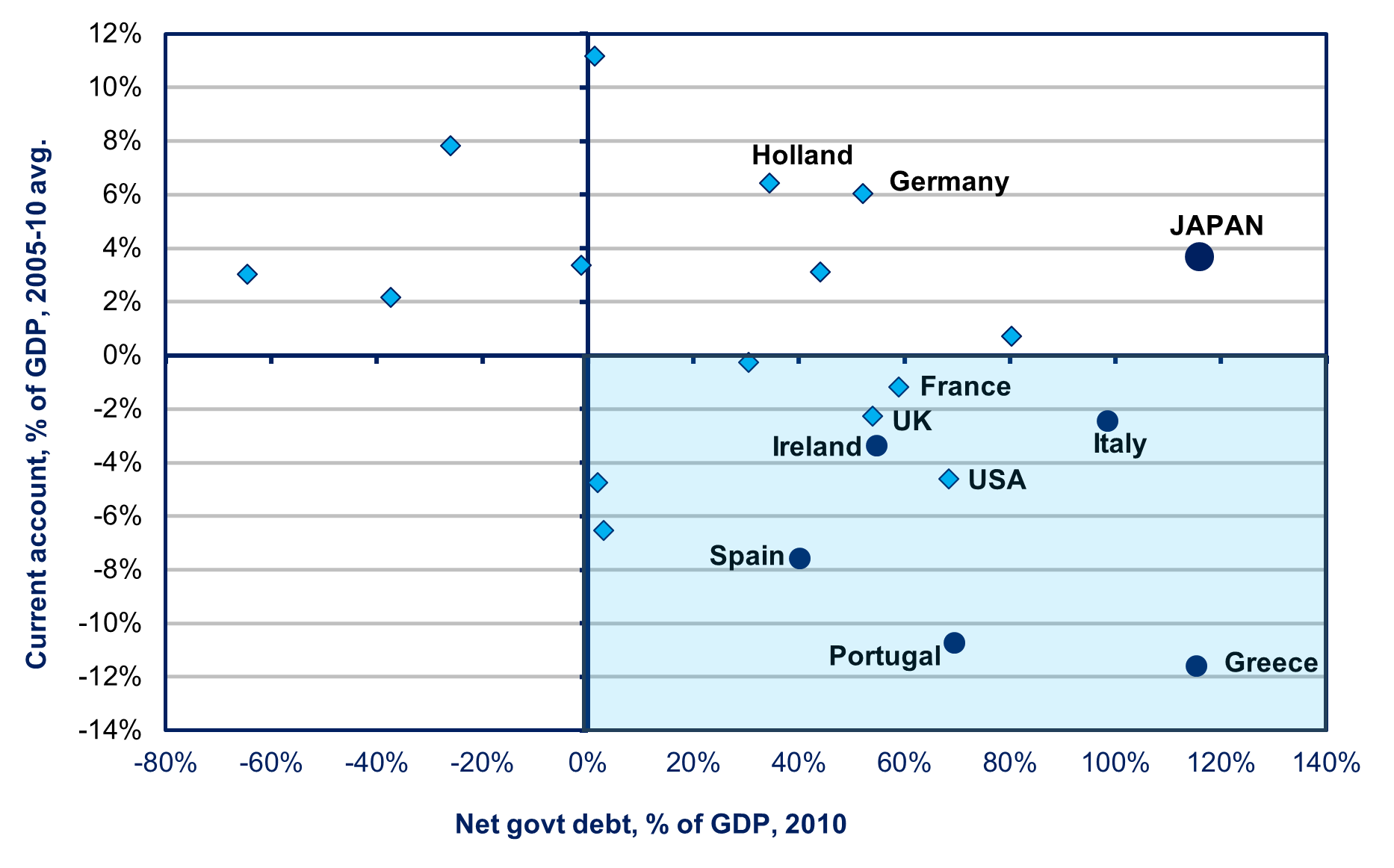

Source: OECD Economic Outlook Statistical Annex 2011 at https://www.oecd.org/content/dam/oecd/en/publications/reports/2011/05/oecd-economic-outlook-volume-2011-issue-1_g1g11686/eco_outlook-v2011-1-en.pdf Note: See third paragraph for explanation of the chart.

Here we go again. Ahead of next month’s Upper House election in which the opposition has made a temporary consumer tax cut a leading issue, Prime Minister Shigeru Ishiba repeated the fiscal hawks’ go-to tactic of catastrophe-mongering. “Our country’s fiscal situation is...worse than Greece’s,” he told the Diet, referring to the 2010 capital flight that triggered the Eurodebt crisis and severe recessions in five afflicted countries.

This is hardly the first time authorities have sensationalized the issue. On the contrary, as I’ll detail below, the Ministry of Finance (MOF) has been sounding false alarms for a half-century. In 2010, it induced Democratic Party of Japan (DPJ) Prime Minister Naoto Kan to tell voters during another election that, if Japan didn’t raise the consumption tax rate, it could become the next Greece within one to two years. The voters didn’t buy it, and the DPJ lost a pivotal Upper House election.

The voters aren’t buying the scare story this time either. Nor should they. As shown in the chart at the top, the only European countries to suffer a crash in 2010 were those with twin deficits. They had not only lots of internal government debt but also a very high current account (trade) deficit. It was the latter that made them vulnerable to capital flight by foreign investors. These are Portugal, Ireland, Italy, Greece, and Spain in the lower right quadrant. By contrast, not a single country with an international financial surplus suffered a crash, no matter how high its internal debt (those in the upper right quadrant, where we also find Japan).

Far from inciting a crisis, eradicating the 8% consumption tax on food would boost GDP by 0.4% and eliminating the tax on all items would boost GDP by 2%, according to the Nomura Research Institute.

Voters Want A Tax Cut, But Also Want It Financed To Avoid Social Welfare Cuts

Voters hit hard by soaring prices, especially for import-intensive food and energy (see chart below), overwhelmingly support a tax cut, while overwhelmingly turning a thumbs down on Ishiba’s plan to hand out cash. And yet, the opposition is not benefiting from this attitude, partly because, in my opinion, they’re making a crucial mistake: not saying how they’d pay for the cut.

Source: https://www.e-stat.go.jp/en/stat-search/file-download?statInfId=000032103842&fileKind=1 Note: Numbers in parentheses are the share of household spending

In an April 21st Asahi poll, voters supported a cut by a 59% to 36% margin. In the May 19th poll, 68% said that they’d be inclined either “very much” or “to some extent” to vote for a candidate or party that supported a tax cut.

Plans vary among the parties, and there are also divisions within each party.

The leading opposition party, the center-left Constitutional Democratic Party (CDP), proposes to eliminate for one year only the taxes on food, now at 8%. Earlier, a 70-member group within the CDP proposed eliminating the tax on food for as long as high inflation lasts. However, party leader Yoshihide Noda did not want any cuts at all. As DPJ Prime Minister in 2012, he had pushed through a tax hike, which led to the DPJ’s landslide defeat in that year. However, Noda was forced by backbenchers to propose at least something. The Osaka-based Japan Innovation Party (JIP) wants to eliminate the tax on food for two years.

The center-populist Democratic Party of the People (DPP) aims to halve the tax on all items, not just food, from 10% to 5% for two years. Finally, the left-populist Reiwa Shinsengumi party advocates for abolishing the consumption tax altogether, an idea that garnered a surprisingly high 20% approval rate in the aforementioned May poll.

Within the LDP, there’s a big split between the backbenchers and the leaders. Eighty percent of its Upper House members support a cut, despite the leadership's adamant opposition. The LDP's coalition ally, Komeito, was expected to propose some sort of cut in its election manifesto but ultimately decided not to do so.

While opposition proposals gain high support, only 28% of poll respondents support Prime Minister Shigeru Ishiba’s plan for cash handouts to families. And only 18% approve of his overall approach to high prices.

And yet, the opposition has not reaped the expected benefits from its stance, despite the cost of living being a top issue in the election. Polls are very fluid, with support for the LDP going up and down. Half the voters want the LDP to lose its Upper House majority (having lost its Lower House majority last year). But you cannot beat someone with no one and the LDP remains the most popular party. The outcome remains very uncertain despite the opposition’s ideas on cost of living issues having more support than the LDP’s.

Here’s one factor. While voters want a tax cut, they also want a substitute form of revenue, fearing that, otherwise, the government could make further cuts to social security, healthcare coverage, and the like. In the above-cited April poll, 60% of respondents feared this outcome either “very much” (18%) or “to some extent” (42%). In a Nikkei poll, 55% favored keeping the consumption tax rate unchanged if that was necessary to secure funding for social security.

This fear is warranted, as the government has already reduced social security benefits for seniors from ¥2.9 million ($20,000 at today’s exchange rates) in 1995 to just ¥2.1 million ($14,500) now, a 30% decrease in price-adjusted terms (see chart on social security in this post). In addition, government spending on healthcare for each person over the age of 65 has been reduced by almost a fifth over the past 30 years (see chart below).

Source: MHLW https://www.mhlw.go.jp/english/database/db-hh/xlsx/5-27e.xlsx, etc. Note: Nominal spending deflated by the medical care price index

To fend off such austerity, 60% of those supporting a tax cut want proponents to explain how they’d make up for the lost tax revenue (almost 1% of GDP if only food taxes are eliminated). Yet, the opposition parties refuse to answer this question. I believe this is a grave mistake, as a ready solution exists: rolling back corporate tax cuts.

(For updates on election prospects, see Tobias Harris’ blog, such as this one.)

Rolling Back Corporate Tax Cuts

A substantial portion of the consumption tax could be eliminated with no loss of revenue just by rolling back the hefty cuts in corporate taxes over the past few decades. In the early 1990s, taxes amounted to around half of corporate profits, but these days it’s only 15-18%. Companies promised that, in return for these tax cuts, they’d invest more in Japan. Yet, they have not done so. While their wage suppression has boosted their profits, it has also reduced opportunities for profitable investment in capacity expansion. So, almost half the cash they rake in lies fallow in their digital vaults (see chart below).

https://www.mof.go.jp/english/pri/reference/ssc/historical/all.xls\

So, here’s the outcome. On the one hand, profits have doubled from 8% of GDP to 16%; on the other hand, corporate tax revenue has tumbled from 4% of GDP to 2.5% (see chart below). Suppose that Tokyo restored the corporate tax rate to its 1990 level. That would increase government revenue by almost 6% of GDP (8.2% vs. the actual revenue of 2.5%). This increase alone is more than the entire consumption tax revenue, which is around 5% of GDP (see the chart below again). And since the tax cuts didn’t boost investment, rolling them back would not lower investment.

Source: OECD at https://tinyurl.com/54pvtk3z

A large number of Diet members support such a rollback to finance the consumer tax cut. However, their party leaders will not hear of it.

Postscript: There Ain’t No Wolf At The Door

Here’s a riddle: for how long has the MOF been “crying wolf” about a fiscal crisis and bond market crash? The answer? A half-century. The first Jeremiad came in 1975 when the Finance Minister issued a “Declaration of Fiscal Crisis,” because Japan did what other countries do during a severe recession: it ran a budget deficit. Then, in 1978, as the MOF began campaigning for a new tax on consumption, another Finance Minister said Japan would “collapse” unless it raised taxes and cut spending.

A “crisis” that has been going on for a half-century is no crisis at all. It is, instead, a long-simmering problem. It manifests itself not in an implosion of Japan Government Bonds (JGBs) but by exacerbating the slowdown in growth. Investors got a costly lesson in the falsity of sensational propaganda in the early 2000s, when they suffered gargantuan losses on short-selling JGBs, which therefore became known as “widow-makers.”

While Japan’s chronic deficit cannot be ignored, it is less a cause of economic problems than a symptom. With both consumer spending and business investment so anemic, the government has had to act as “buyer of last resort” for decades just to keep the economy afloat.

In any case, who is going to flee JGBs today? Certainly not the Bank of Japan (BOJ), which owns almost half of all JGBs (see chart below) and whose purpose is to shore up the country’s finances. Nor Japanese banks, corporations, and insurers, who need stable finances. Only 13% of JGBs are owned by foreign investors, and many have learned not to tangle with the “widow-maker.”

Source: BOJ and MOF

Alarmists seized on the poor reception of a recent auction for 30-year and 40-year JGBs, leading clickbait headlines. However, Bank of Japan (BOJ) officials say the episode in superlong bonds was due to technical factors unrelated to the overall level of government debt. There is no spike in the benchmark 10-year JGBs. On the contrary, yields today are lower than a few months ago.

As part of their crisis-mongering, the MOF and LDP point to Japan’s gross government debt, which now stands at 2.35 times GDP. However, gross debt includes what one government agency owes to another, and that’s a misleading measure. What counts for vulnerability is the portion held by private investors (net debt). That amounts to 1.34 times GDP, and the IMF does not see it rising at least through 2030, the last year in its forecast. If there was no JGB crash a decade ago when net debt was even higher, why should there be one now?

Source: https://www.imf.org/-/media/Files/Publications/WEO/WEO-Database/2025/april/WEOApr2025all.ashx

Moreover, as long as the government can borrow, there is no crisis. The truth is that interest payments as a share of GDP have fallen from 2% in the mid-1980s to just 0.4% this year.

.Yes, interest rates are rising somewhat, but so is inflation. As long as real (inflation-adjusted) interest rates do not rise much—they are still negative today—then neither will interest payments relative to GDP.

Next time you hear Japan’s fiscal hawks speak in the language of Greek tragedy, consider the source.

To receive new posts and support my work, consider becoming a free or paid subscriber.