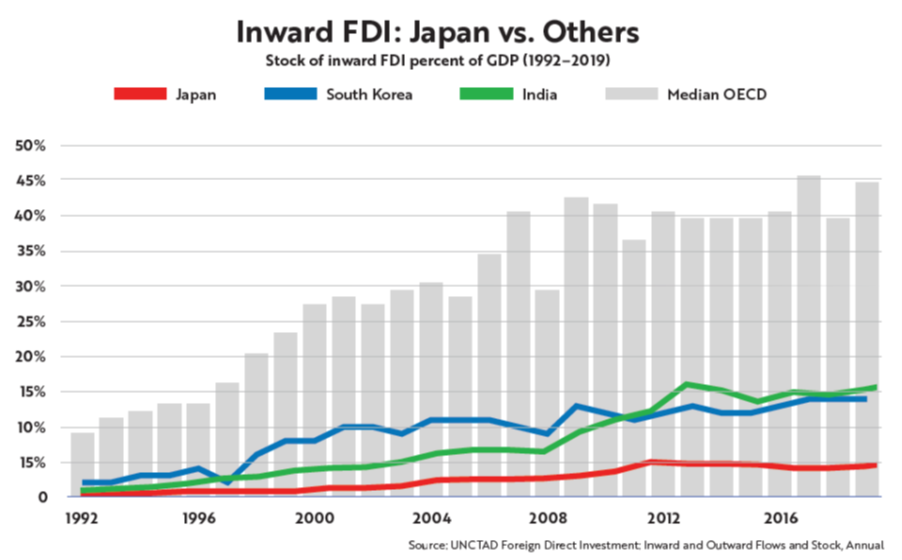

Will Corporate Governance Reforms In Japan Lead to More Inward FDI?

How American Execs in Japan See the Situation

Many, perhaps most, American business leaders in Japan believe that corporate governance reforms in Japan could lead to more acquisitions of healthy Japanese businesses by foreign companies. The governance reforms promulgated under Shinzo Abe, they believe, add to reforms in the Koizumi era that had already made inbound M&A a lot easier. Some of these Americans played an important role in helping to shape both the Koizumi-era and Abe-era reforms. The Journal—published by the American Chamber of Commerce in Japan (ACCJ)—just published a piece by me on this topic (see PDF link below). It adds to what I’ve published before on the issue of inward FDI.

Here’s their chain of logic . A series of corporate governance reforms is putting pressure on Japan’ corporate giants to pay more attention to profitability, not just sales, market share, and empire-building. To become more efficient and profitable, the big overly-diversified corporate giants will have to shed operations that may be profitable in themselves but detract from the overall efficiency of the conglomerate and could perform much if they were either independent or part of a different firm.

In this piece, I argue that this logic may eventually prove to be true, but it has not made much of a difference so far either in regard either profitability, or to the pace of divestment, or in sales to foreign strategic buyers.

1) Companies may claim that they’ve adopted a “select and focus” streamlining approach, but the data says such cases are exceptions.

2) According to a report by Private Equity (PE) giant Bain, companies have not hived off profitable divisions and subsidiaries even if they detract from the firm’s overall strategic position. They are getting rid of unprofitable but, it remains to be seen whether that will lead to a broader focus on core competencies.

3) While some governance reforms have been implemented by some companies, on the whole they have not yet led to better corporate efficiency as measured by Return, On Assets (ROA), i.e. profits in ratio to assets. On the contrary, much of the ostensible improvement in corporate efficiency is simply a result of the Bank of Japan artificially boosting profits as it pushes interest rates lower and lower. It is, in effect, shifting wealth from household savers to corporate balance sheets.

As the chart above shows, if companies use current (i.e., profits after interest payments) to measure return on assets (ROA), it looks as if their performance has improved. However, when ROA of the 5,000 biggest firms is measured in terms of operating profits—i.e., profits before interest—ROA in 2014-2019 (pre-Covid) is lower than it was in the mid-2000s. If shareholders accept this rose-colored image of profitability and efficiency, managers do not face a big incentive to hive off healthy, but incompatible, units.

4) Over the last decade or so, tcases of corporations selling parts of themselves to foreign firms or PE funds have not increased in either number or value. This relative stasis is disguised by the fact that, in certain years, there have been huge one-off rescue operations for firms needing a rescue operation. Toshiba’s $18 billion sale of semiconductors unit to a consortium led by Bain in 2018 is a recent example.

Here’s the article. It’s got several helpful charts to illustrate the points.