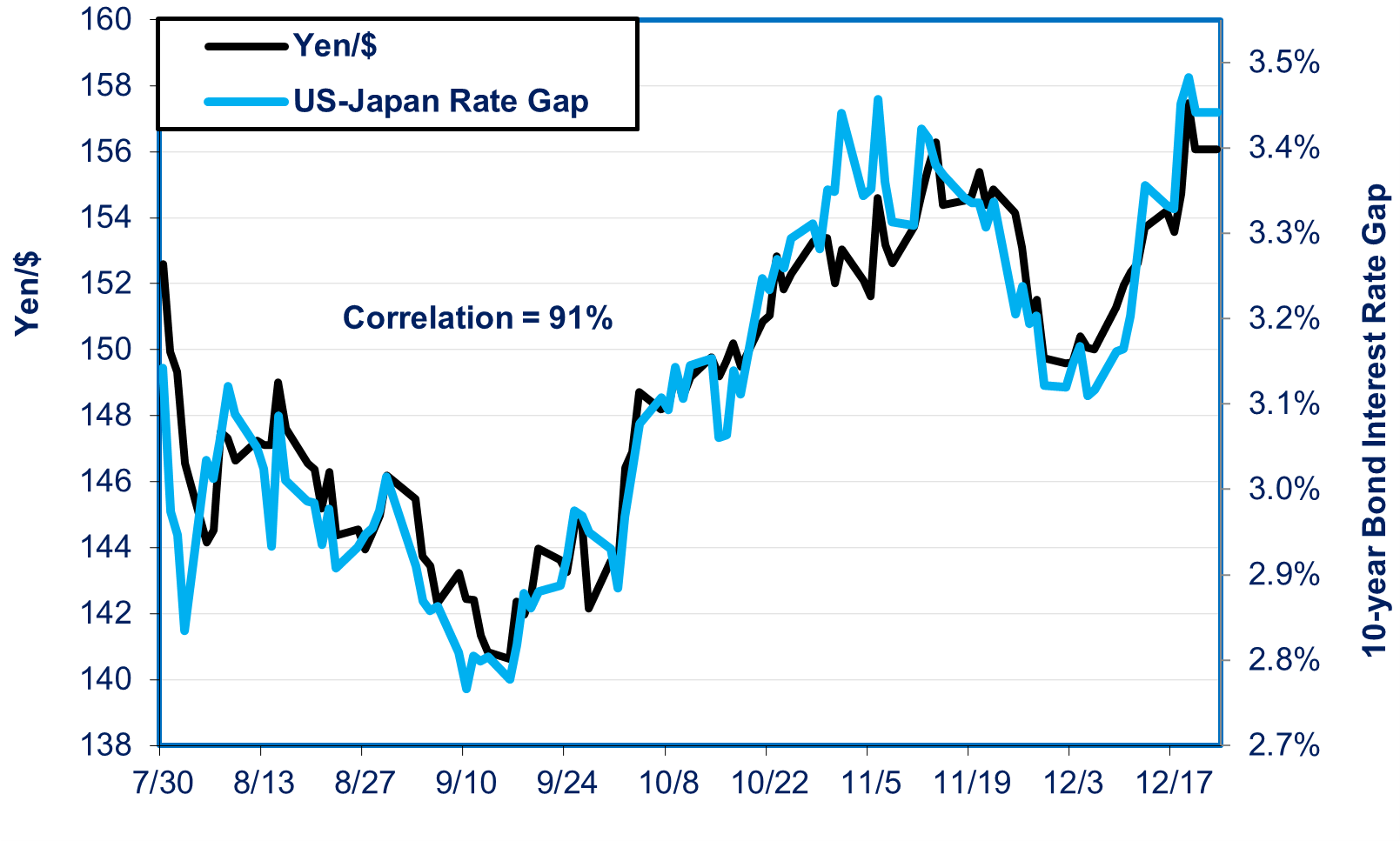

Yen at ¥156/$ Thanks To Expected Trumpflation

Fed and BOJ Both Retreat on Interest Rate Moves

Source: Based on data from Wall Street Journal

A big drop in the yen and a pause in interest rate hikes by the Bank of Japan (BOJ) are the first visible impacts of Donald Trump’s return to the White House on Japan. If Trump implements the tariffs and tax cuts as steeply as he vowed during the campaign, the shock to Japan’s economy will be even greater, as I suggested earlier this year.

The impact on the yen is quite straightforward. A variety of Trump’s policies are highly inflationary: big tariff hikes, big tax cuts, and higher budget deficits. To counter this, the Federal Reserve has to keep interest rates higher, which will lure money to the US, strengthening the dollar and weakening the yen. Anticipating this higher inflation, the Federal Reserve not only failed to raise interest rates on Wednesday, it also predicted that it would likely cut rates only twice in 2025 instead of the four times it had predicted just three months ago. All of this caused a sharp hike in US 10-year government bond yields. That, in turn, led to a substantial increase in the gap between American and Japanese interest rates. As seen in the chart at the top, since late July, there has been a 91% correlation between the ups and downs in the interest rate gap and the ups and downs of the ¥/$ ratio.

The Fed now projects that it will take longer to bring inflation down to 2% than it had projected in September (2027 instead of 2026) and that it will take higher interest rates to bring it down. So, for 2025, the Fed projected that inflation would be 2.5% rather than the 2.1% it had predicted in September. It also said that the federal funds rate, i.e., the rate on overnight money, will average 3.9% rather than the 3.4% it had projected in September. Otherwise, inflation would be even higher. While 3.9% is lower than today’s rate of 4.25%, it’s still higher than either it or the market had previously anticipated. There are similar changes in its forecast for 2026.

What This Means For Japan’s Inflation and BOJ Policy

Unfortunately for Japan, its financial conditions can be blown about like a leaf in the wind by events in the US. The weaker yen resulting from the Fed’s stance translates into more imported inflation in Japan. That is the main reason why the Bank of Japan (BOJ) failed to lift interest rates in Japan yesterday. This is one of the times that Fed chair Jerome Powell can have more influence over BOJ actions than Governor Kazuo Ueda.

A weaker yen means Japan has to shell out more yen for whatever it imports. That sends skyward the prices for import-intensive items like food, energy, clothing, and footwear. In fact, 76% of Japan’s total hike in prices since 2020 came in those four products, even though they account for just 37% of all consumer spending (see chart below). That has cut real wages for consumers and raised costs for energy among small and medium companies.

Source: https://www.e-stat.go.jp/en/stat-search/file-download?statInfId=000032103842&fileKind=1 Note: the number in parentheses shows the share of these items in the total consumer budget

The BOJ had believed that the higher inflation caused by the weakening yen, as well as the higher global commodity prices caused by Covid and the war in Ukraine, would subside. Conversely, a hike in nominal wages would lead to a rise in domestic demand-created inflation to 2%. As a result, overall inflation would gradually move to its goal of 2%. However, if we look at inflation trends over the past six months (chart below), we can see that inflation in all products other than food and energy stood at 2%. By contrast, prices have been rising at a 5-6% pace in food, energy, clothing, and apparel.

These figures, along with Trumpflation and a weaker yen, are making the BOJ far less confident in its baseline. So, at least for this month, the BOJ is waiting until more evidence comes in.

The BOJ faces a dilemma. Normally, expectations of higher inflation in Japan would cause the BOJ to raise interest rates. That would not only narrow the rate gap—and thus counter the downward pressure on the yen—it would also fight the expected inflation. On the other hand, the weaker yen and other factors have been reducing real wages and, thus, consumer spending for most of the past five years (see charts below). That weakens economic growth, and the BOJ needs to keep rates low to keep the economy afloat.

Source: https://www.mhlw.go.jp/english/database/db-l/r06/2410pe/xls/fu2410pe.xlsx

Source: https://www.esri.cao.go.jp/jp/sna/data/data_list/sokuhou/files/2024/qe243_2/tables/gaku-jk2432.csv Note: The decline in real consumer spending since 2014 results from stagnant, and sometimes falling, real income. That is due to the two hikes in the consumption tax, the big depreciation of the yen, cuts in government spending on social security per senior, and wage austerity by Japan’s companies.

In short, some of Japan’s problems call for higher interest rates, and some call for lower rates.

To make matters worse, it’s uncertain how much and when Trump will implement the policies he campaigned on. On the domestic front, it’s unclear whether the relatively high nominal wage hikes that employers granted this year will be repeated next year. Nor is it clear how nominal hikes will translate into real wages because the severity of imported inflation remains unclear. The BOJ’s entire inflation strategy depends on keeping nominal wage hikes at 3% per year, with the hope that this will lead to hikes in real wages. It will take several months to see the wage picture for fiscal 2025. So, at least for this month, the BOJ is adopting a wait-and-see attitude.

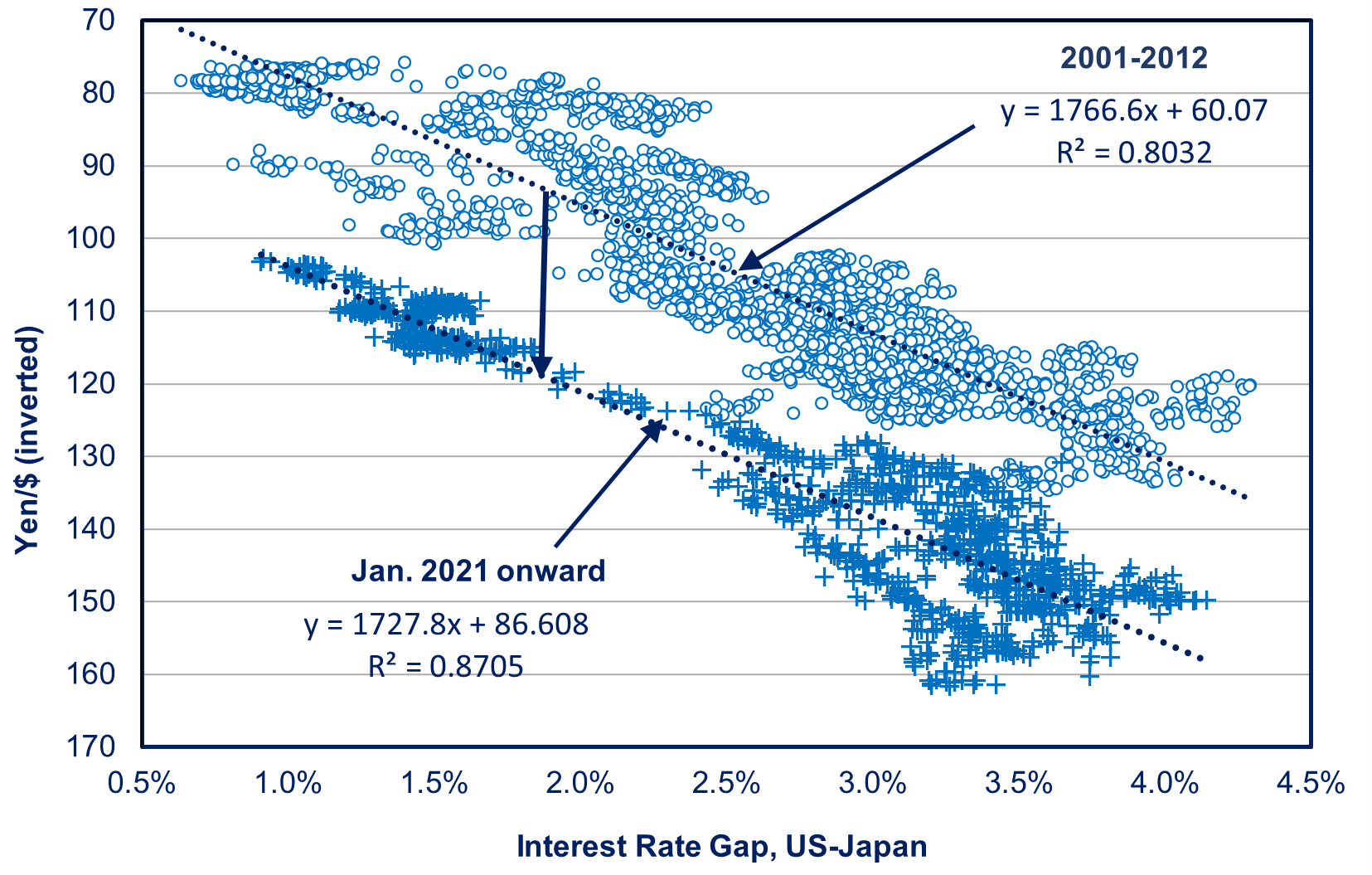

The Yen’s Long-term Prospects

As I noted in the chart at the very top, in the short term, the interest rate gap is the primary determinant of the ¥/$ rate. By contrast, in the long-term, the yen’s purchasing power depends on the fundamentals of the economy, such as productivity growth, inflation compared to other countries, the balance of payments figures, and so forth. Unless those fundamentals improve, the yen will remain quite weak.

To see the long-term deterioration in the yen’s value, consider the chart below. We can see two trend lines vis-à-vis the ¥/$, the higher one covering 2001-12 and the lower one showing the period since January 2021. The slope of each trend line shows how much the yen moves in tandem with changes in the interest rate gap. However, the vertical drop signified by the downward arrow between the two trend lines shows us the long-term decline in the yen’s purchasing power, e.g., how many yen it would take to buy a barrel of oil or a ton of wheat even if their dollar prices remained the same. What it tells us is that, at any given gap between American and Japanese 10-year government bond rates, the yen is about 25 points weaker today than it would have been two decades ago. At today’s rate gap of around 3.5%, the yen’s value was typically around ¥121 two decades ago. Today, at that same rate gap, its forecast value is about ¥146. Since the yen fluctuates around that forecast due to factors other than the rate gap, its actual value today is around ¥156. The bottom line is that, even when the rate gap shrinks, the yen is not going to recover the value it had two decades ago. The yen is weak because Japan’s economy is weak, and the competitive power of Japan’s exporters has deteriorated. Monetary policy cannot fix that.

Source: Author calculations based on Wall Street Journal data

Thank you for another extraordinarily clear explanation of the factors -- both short and long term -- behind the current Yen/USD exchange rate.

While there is probably little that Japan can do to increase its dependence on foreign food supplies, it seems that such an approach might help in the long run.

In any case, continuing to invest in U.S. stocks and other U.S.-based financial products certainly seems like the safest bet for the foreseeable future.

Very interesting post. In particular the last graph is very telling. However, I noticed data from between 2012 and 2021 was omitted. I imagine there was some weird stuff going on with the Great Recession, etc. but would be interesting to see.

I agree, Japan is in a pickle because it has essential become subservient to the US economically and therefore can't fully take on economic headwinds when they arise as they can't control US economic decisions. Do you think it will ever be possible for Japan to have more control of their economic future? What would have to occur?