My Financial Times Oped On The Yen

Japan’s currency is so weak because exporters have lost their competitiveness

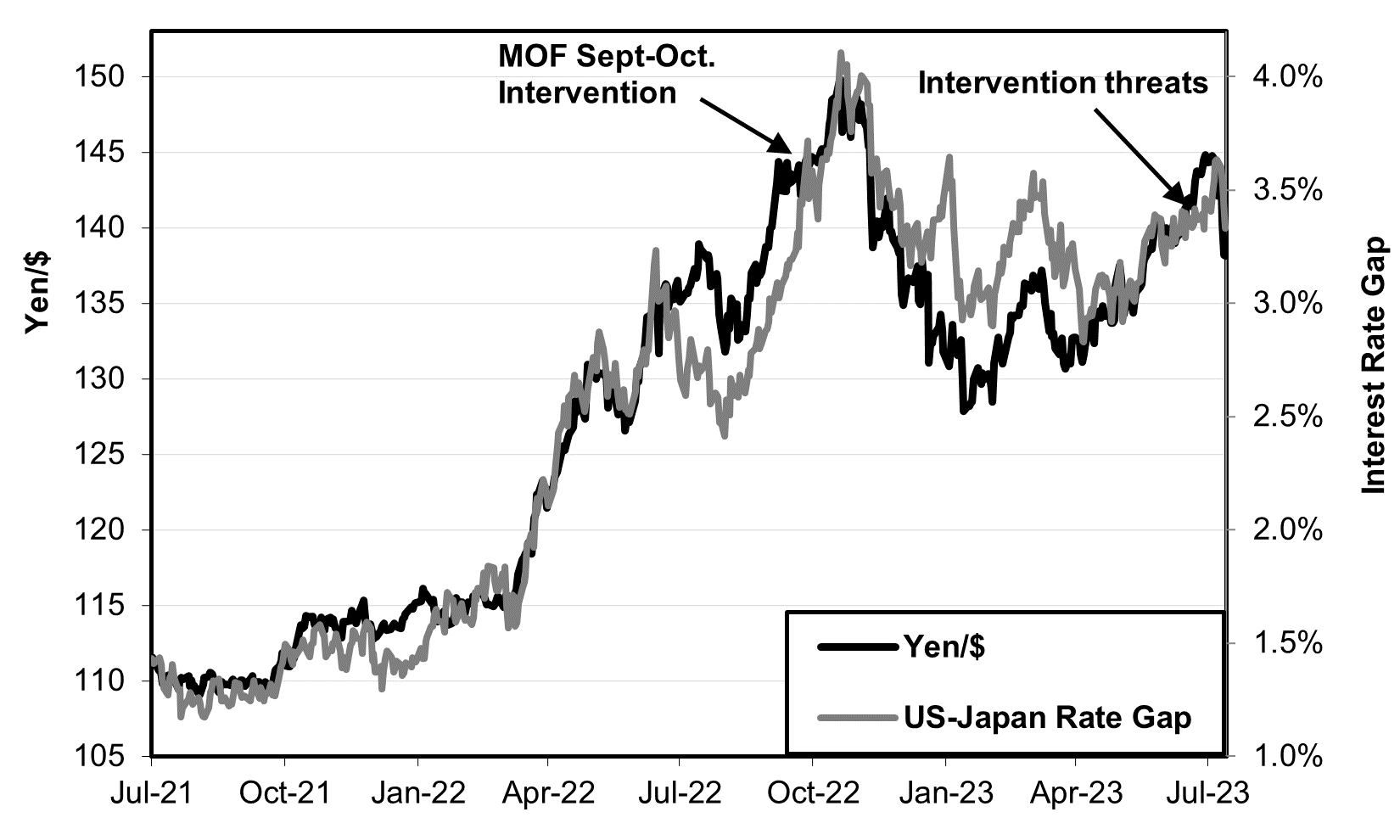

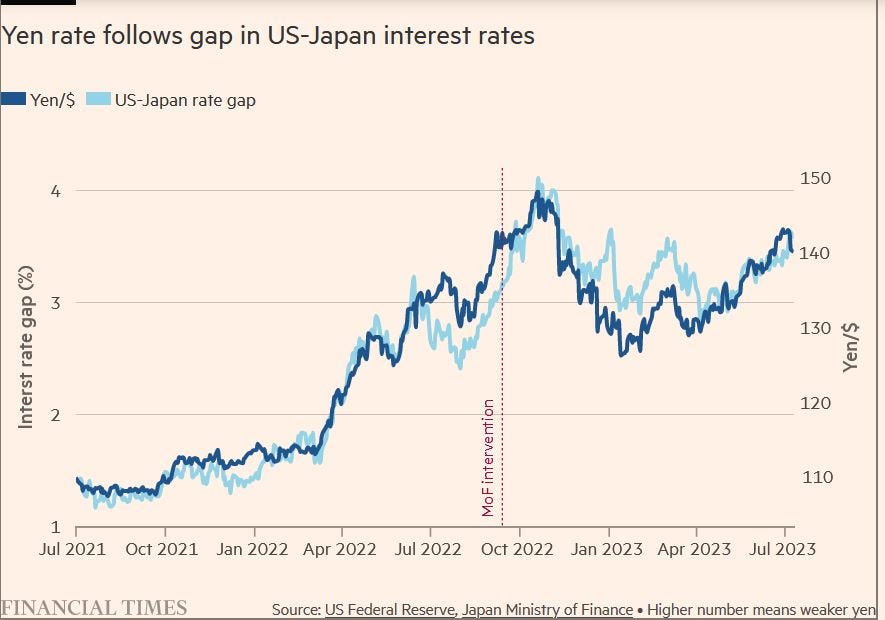

On Wednesday (July 12), the Financial Times published a guest column by me on the yen’s weakness. The recent gyrations of the yen show how much, and how quickly, its value depends on changes in the interest rate gap between US and Japanese 10-year bond yields. When I wrote the column, that gap was rising, and, as a result, the yen was weakening so fast that the Japanese Finance Ministry was threatening intervention to shore it up. By the time it was published, three news events caused the rate gap to narrow, which, in turn, caused the yen to regain some of its lost value (see chart updated from the one published in the FT).

Source: Ministry of Finance, Federal Reserve Board

In the US, weaker-than-expected jobs growth and a bigger-than-expected decline in inflation led the market to expect that the Federal Reserve would not raise interest rates as much as the market previously expected. That changed anticipation led to a fall in the 10-year Treasury bond. In Japan, a misreading of the May wage figures led to expectation by some players that the Bank of Japan might let interest rates rise sooner than previously expected, perhaps as early as its meeting this month. I’m not a professional forecaster, but I’d be surprised if the BOJ moved that quickly.

Here’s the text of the FT column. For those with a subscription, click here.

Intervention to shore up the yen will not work

Japan’s currency is so weak because exporters have lost their competitiveness.

The yen has weakened so much that, once again, Japan’s ministry of finance is threatening to intervene in currency markets to shore up its value. If it does so, it is bound to fail, just as it failed last year despite spending a stupendous ¥9.19tn, almost 2 per cent of gross domestic product.

Intervention only works when a currency is out of line with economic fundamentals, but that is not the case today. The yen is so weak — worth 25 per cent less than two years ago — because Japan’s exporters have lost their past competitiveness. In fact, if current trends continue, Japan may be overtaken by Korea in the real (price-adjusted) volume of exports.

A few decades back, Japan’s consumer electronics, industrial machinery and automobiles were so clearly superior that its exporters could command high prices and still enjoy a high share of global exports. Today, however, these companies have shed much of their lustre. To sell their products, they must lower their prices, which requires a weaker yen.

In fact, the “real effective yen” is the weakest it has been in a half-century, according to the Bank of Japan. That measure takes into account the difference in price trends between Japan and all its trading partners. As a result, the real effective yen indicates how the prices of Japanese products in foreign markets compare with those of competitors.

Over the past two years, the main factor in the yen’s value has been the gap between 10-year government bond rates in the US and Japan. When Treasuries pay much more than Japanese government bonds, investors sell the latter and therefore the yen itself, in order to buy dollars as they purchase US debt. That selling pressure lowers the value of the yen.

In fact, since July 2021, there has been a stunningly high 97 per cent correlation between daily ups and downs in the rate gap and daily moves in the yen-dollar rate. The MoF intervention last autumn could not alter this linkage, nor would it today. At present, the interest rate gap is fluctuating around 3.5 per cent and a yen that recently weakened to ¥145 a dollar is in line with that gap.

If the interest rate gap were the sole cause of the weak yen, then a rise in Japanese bond rates and a fall in US rates could cure the problem. In reality, the yen is not likely to return to levels deemed normal a decade or two ago. On the contrary, an interest rate gap that yielded a ¥100 per dollar exchange rate back in the early 2000s now translates into around ¥120 per dollar.

The reason is that, even with a cheap yen, Japanese companies have trouble competing with exports. For the 30 years to 2010, whether the yen was strong or weak, Japan ran trade surpluses every year but one. Since 2011, however, the country has suffered trade deficits in nine of the past 12 years, even though the real effective yen during the last decade was 25 per cent cheaper than it was during 1980-2010. While in the short-term, income from Japan’s foreign investments acts as a counter to weakness, the longer-term direction of the yen must reflect the trade weakness.

Japan’s share of price-adjusted exports by rich countries peaked at 8 per cent back in 1985. Over the succeeding decades, the share steadily dropped to just 5.8 per cent, despite the steady weakening of the yen. By contrast, both the US and Germany maintained their share.

In 2000, Japan’s electronics companies enjoyed a trade surplus equal to a hefty 1.3 per cent of gross domestic product; now the sector regularly runs trade deficits. In autos, Japan will soon be overtaken by China as the world’s top exporter, partly because Japanese companies lag in battery-powered electric vehicles.

The auto case brings up another reason a weak yen has not helped Japan’s exports as much as policymakers had hoped. Japan’s carmakers make more than 80 per cent of their overseas sales by producing overseas rather than exporting from Japan. The same pattern is seen in electronics, machinery and other products. The more Japanese companies move their production overseas, the smaller the boost to exports for any given drop in the value of the yen.

One final point: a weak yen means Japanese households and producers have to pay more for foodstuffs and energy. And it leaves consumers with less money to buy products made in the country. As a result, real (price-adjusted) household spending in 2023 is no higher than it was way back in 2012. The weak yen doesn’t just reflect economic weakness; it also makes a weak economy even shakier.

The writer is the publisher of Japan Economy Watch and author of the forthcoming book ‘The Contest for Japan’s Economic Future’

Copyright The Financial Times Limited 2023. All rights reserved.

Thanks for providing your perspective--especially on the "free side" of a paywall. As a long-term resident of Japan now with permanent residency status and the intention to remain based in Japan forever, I read your prognosis with great interest. I tend to share your viewpoint, but I am still weary of not hedging my bets for a return to the days of a much stronger yen vs. the USD. Although I spent a few "tours of duty" living and working back in my native Chicago, I have lived in Japan during periods when the fx was right around current levels as well as when it was as high as 80 yen/USD. Especially considering the effect of demographics and the factors you cited, it does seem unlikely that Japan, Inc. will ever again be able to export its way out of a weak yen. It's just difficult to fathom the likelihood that Japan's economy (and the relative value of the yen) will simply deteriorate slowly during the rest of my days here. Glad to be invested heavily in the US stock market!

It was a brutally honest article but I have seen more brutal articles coming from Japanese experts. I understand that you hold your firepower because you want to save faces for the Japanese.