Reading the Mind of BOJ Chief Ueda

Countering Market Views That He Cannot Do What He Says

Source: https://www.e-stat.go.jp/en/stat-search/file-download?statInfId=000032103932&fileKind=1

[This is what I believe Bank of Japan Governor Kazuo Ueda thinks about critics who say he will be compelled to raise interest rates in the near future. Some is based on public information, some on my conversations with people in the know, and some is surmise on my part based on how BOJ statements relate to certain economic trends. Anything in quote marks is genuine. As with my January post on reading the mind of Haruhiko Kuroda. my purpose is to show why Ueda thinks current policy is both correct and sustainable.]

I don’t understand why many major players in the financial markets are still telling their clients and the press that I will raise interest rates during the coming months, even though I’ve repeatedly declared that I will not. Here’s a typical example from a former top BOJ economist named Seisaku Kameda, who told Reuters soon after I became Governor, “Wages are rising and domestic demand is firm...The BOJ may see scope to tweak YCC as early as June.” YCC (yield curve control) refers to our policy of setting rates, not just for overnight instruments like other central banks, but for notes and bonds of all maturities. Without YCC, long-term interest rates would rise. I’m not going to do that any time soon, certainly not just a few weeks from now.

A Reuters poll taken April 12-19 showed over half of economists predicted an end to YCC control by year-end. So, I’ve had to repeat my message and make it even more firm. In my May 19 press conference, I again pointed out that today’s high inflation in Japan is a result of temporary factors. So, it would hurt the economy to raise interest rates as if high inflation were going to last. “The cost of prematurely shifting policy, and nipping the bud towards achieving 2% inflation, is extremely large. It's appropriate to take time to judge when to tweak ultra-easy policy toward a future exit...It will take time to shift public perceptions that prices and wages won't rise much.” Until those perceptions shift, and wages actually rise, we won’t enjoy 2% inflation on a sustained basis.

In our April 28 “Outlook” report, the BOJ Board projected that our measure of core inflation—all items minus fresh food and energy—would have risen 2.2% in fiscal 2022 (which ended March 31st, 2023), then will accelerate to 2.5-to-2.7% in fiscal 2023, and finally fall back to 1.5-1.8% in fiscal 2024.

Yes, we could be wrong. Prices could keep rising faster than we expect. But policymakers always have to figure out how to balance risks. What is the harm if we tighten rates too late vs. the harm if we tighten rates too early? As I said, “The cost of waiting to ensure inflation is sustainably at 2% is smaller than shifting policy prematurely.” That’s because it’s easier to curb inflation than to overcome deflation.

Can the Market Force My Hand?

Critics believe that events beyond my control in terms of inflation and market turmoil will force my hand. They felt the same thing regarding my predecessor last fall. They were wrong then and they’re wrong now.

In fact, I’m under less pressure than Kuroda. During his tenure, the bank set the maximum rate on 10-year government bonds (JGBs) at 0.25%. Because the majority of market traders felt sure he would have to raise rates, they sold JGBs, which caused rates to rise. The BOJ had to spend a lot of money buying JGBs to fight this pressure. Finally, like releasing a pressure valve, Kuroda lifted the 10-year rate ceiling to 0.5%. Lots of market players believed that, having forced Kuroda to do that once, they could force him to do it again to, say, 0.75%. That never happened. His tactic worked. Since then, the 10-year rate has fluctuated around 0.4%. This tells me that the majority of traders realize that the BOJ has the power to sustain its policy; they fear losing money if they bet against us.

Consequently, the tide of opinion is changing. For example, Shigeto Nagai, head of Japan economics at Oxford Economics, recently told clients, “Ueda’s game plan appears to have a longer time frame than we had thought We believe it is more likely that the status quo will continue in the coming quarters.”

Japan’s Inflation is Temporary “Cost-Push” Unlike US and Europe

Here’s what the critics don’t get. Central bankers distinguish between two kinds of inflation: cost-push vs. demand-pull, and, unlike the US and Europe, Japan is mainly suffering from the former. By contrast, demand-pull happened in the US because the government gave consumers and companies so much cash to fight a possible recession arising from Covid.

Japan’s cost-push began when energy and food prices skyrocketed due to Russia’s invasion of Ukraine, and the weakening yen amplified that price shock. When the yen gets weaker, Japanese have to pay more for imports, e.g., having to pay ¥140 for products that sell for $1 in the international market instead of ¥1.25.

As a result, inflation in Japan will recede when international prices come back to earth. The BOJ’s critics believe that price hikes are spreading throughout the economy, and creating expectations of continued price hikes. So, they say, what started as cost-push inflation is now feeding on itself.

But there’s little evidence for that view, at least not so far. Virtually all of the inflation in the last couple of years has arisen from the import-heavy food and energy sector. Inflation in the whole rest of the economy is barely above the 2% level. Moreover, inflation in food and energy has come down a great deal (see chart at the top). Of course, a year from now, things may look very different. But in which direction: higher inflation or lower? No one knows for sure, although the odds are that inflation will peak sometime in this fiscal year. So, the least dangerous course is to wait and see, and carefully follow the data. If the evidence changes, the BOJ can shift, and little will have been lost.

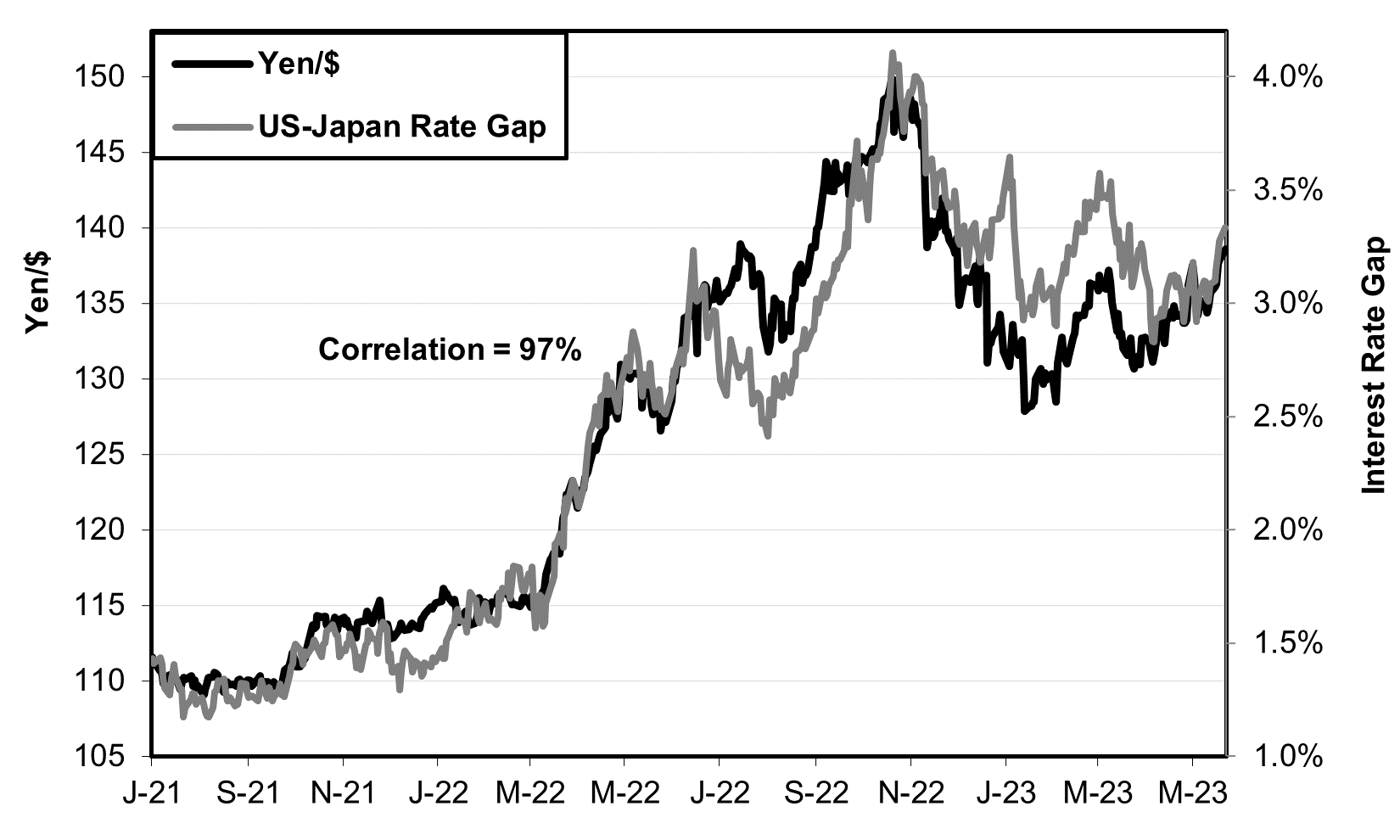

We also have to watch movements in the yen very carefully because it greatly impacts the price that companies and households pay for import-heavy items. Only a couple of months ago, many traders saw the yen strengthening to ¥125/$. But, due to a rise in long-term US interest rates, the yen has weakened again to ¥138 (see chart). The recent rise in US rates may be the result of anxiety over whether the US will raise the debt ceiling. But, if the yen remains this weak, that will place upward pressure on prices in Japan and, depending on how much the yen weakens, and for how long, delay the downshifting of inflation.

The New BOJ View: 3% Nominal Wage Hikes Are Indispensable

Back in 2012, when Kuroda became Governor, he believed that he could create 2% sustained inflation in just two years just by unleashing a “big bazooka” of monetary ease. Monetary stimulus needed no help from fiscal policy or changes in the real economy like wage hikes and such.

That turned out to be wrong and Kuroda adapted. He realized that, while monetary ease was necessary, it was not sufficient. While Kuroda never explicitly acknowledged this shift, his speeches focused more and more on the need for wage hikes. He argued that such hikes were indispensable to create a virtuous cycle of wages, demand growth, and prices.

It will take steady 3% annual growth in nominal wages to produce our goal of 2% consumer price inflation. Here’s the arithmetic. Productivity growth (output per worker) is around 1%. So, if nominal wages go up 3%, then the labor cost to companies to produce a good or service is 2%, i.e., 3% wage hikes minus 1% productivity growth. Companies will pass this 2% hike in their costs onto customers. Workers, in turn, will enjoy a well-deserved 1% growth in “real” wages, i.e., nominal wage hikes of 3% minus inflation of 2%.

One of the main reasons that deflation and then weak price hikes have been so prolonged is that workers have suffered negligible or negative real wages for years. In the past five years, nominal wage hikes came close to 3% only once: in Oct-Dec. 2022. Meanwhile, real wages have fallen for years. In January-March of this year, real wages fell a huge 3.4% from last year (see chart below). One consequence was that household spending in March was down 1.9% from a year earlier. How can consumers spend more, and thereby put upward pressure on prices, if their real income is falling?

Source: https://www.mhlw.go.jp/english/database/db-l/monthly-labour.html

For years, forecasters have predicted that Japan’s labor shortage would create substantial wage hikes due to the laws of supply and demand. That, however, has not happened. Consequently, no one really knows whether or not wages will rise a great deal for the overall labor force just because big companies reached deals for an average of 3.7% wage for unionized workers. The workers involved in the annual “shunto” wage negotiations comprise only a small sliver of all employees. Maybe wages will rise broadly. However, “there is extremely high uncertainty over the sustainability of wage hikes, consumption, and overseas economies.” Let’s wait for data on wages for the workforce as a whole to come in over the next few months.

GDP Recovery Slow

The slow pace of economic recovery is another factor raising doubts about Japan’s future inflation rate. In January-March, GDP was still 1% below the level reached five years earlier in 2018 and only 4% above the average ten years earlier in 2013 (see chart). The economy is still operating below its capacity. A slack economy usually portends less upward pressure on consumer inflation.

Source: https://www.esri.cao.go.jp/jp/sna/data/data_list/sokuhou/files/2023/qe231/tables/gaku-jk2311.csv

Re your comment on wages: official stats are probably accurate for salaried workers but your hourly paid konbini workers (and labourers and housekeepers and and and...) who were paid JPY800/hour 7-8 years ago are now earning JPY1,200 or so depending on the region. Given that the proportion of Japanese in conventional employment has been falling steadily for decades, I'd say that while the salaried middle class are almost certainly feeling the pain of rising prices vs static incomes, actually a large swathe of the population has been well insulated against inflation and if anything is feeling better off.