Stock Rally Does NOT Mean “Japan Is Back”

Stock Prices Driven By Wage Cuts & Record Stock Buybacks

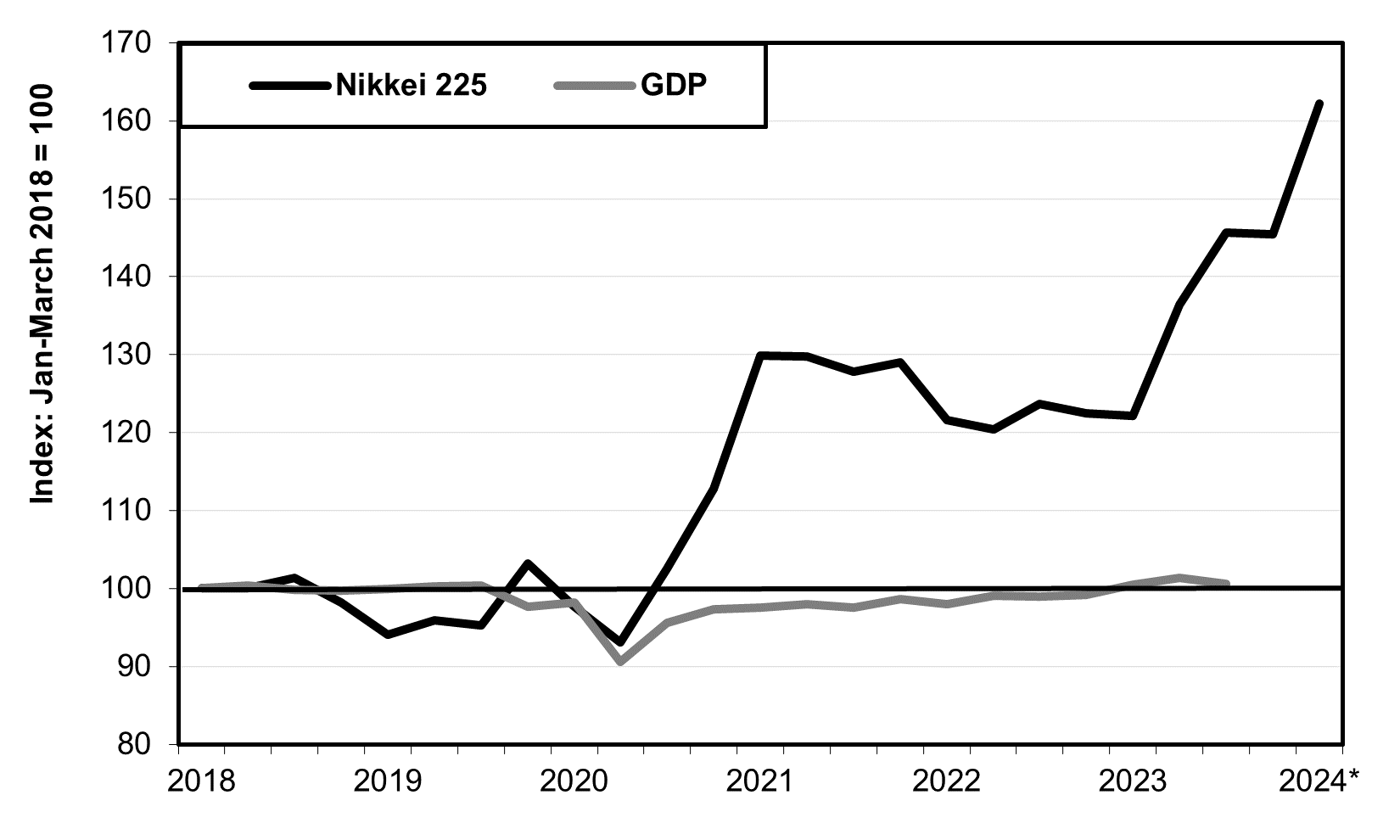

Source: https://fred.stlouisfed.org/series/NIKKEI225 and https://www.esri.cao.go.jp/jp/sna/data/data_list/sokuhou/files/2023/qe233_2/tables/gaku-jk2332.csv

Note: Nikkei 225 shows the average per quarter; 2024 shows the closing price on January 25th

Once in every decade since the bubble burst in 1990, a temporary upsurge in stock prices combined with promises of reform leads stockbrokers, politicians, and some analysts to proclaim, “Japan is back.” In recent weeks, it has become this decade’s turn. However, this boast is likely to be just as illusory as those told during the reigns of Prime Ministers Hashimoto, Koizumi, and Abe.

Under certain conditions, the stock market can both reflect the economy and help predict its future. But those conditions do not prevail in Japan and do not always prevail elsewhere either. While stock prices are up 60% from six years ago, real GDP is up a trivial 1% (see chart above), and real compensation per employee is down 5%.

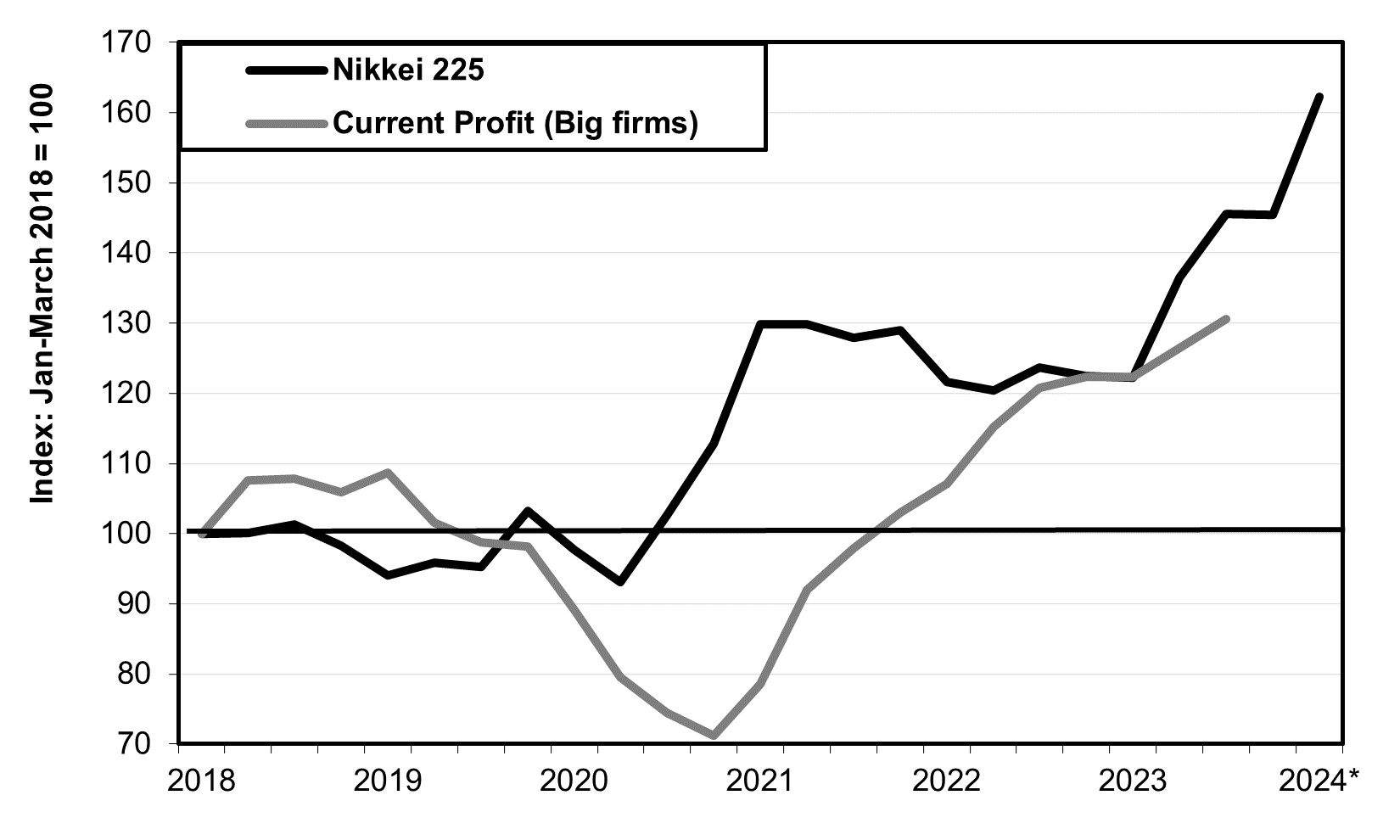

The stock prices do reflect both rising corporate profits in Japan (see chart below) and a flood of stock buybacks (where companies lift the share price by buying back their own shares; more on the latter below).

So, yes, savvy investors may make a lot of money—that’s above my pay grade— but most of the public will see little or no benefit.

How Are Firms Making Profits?

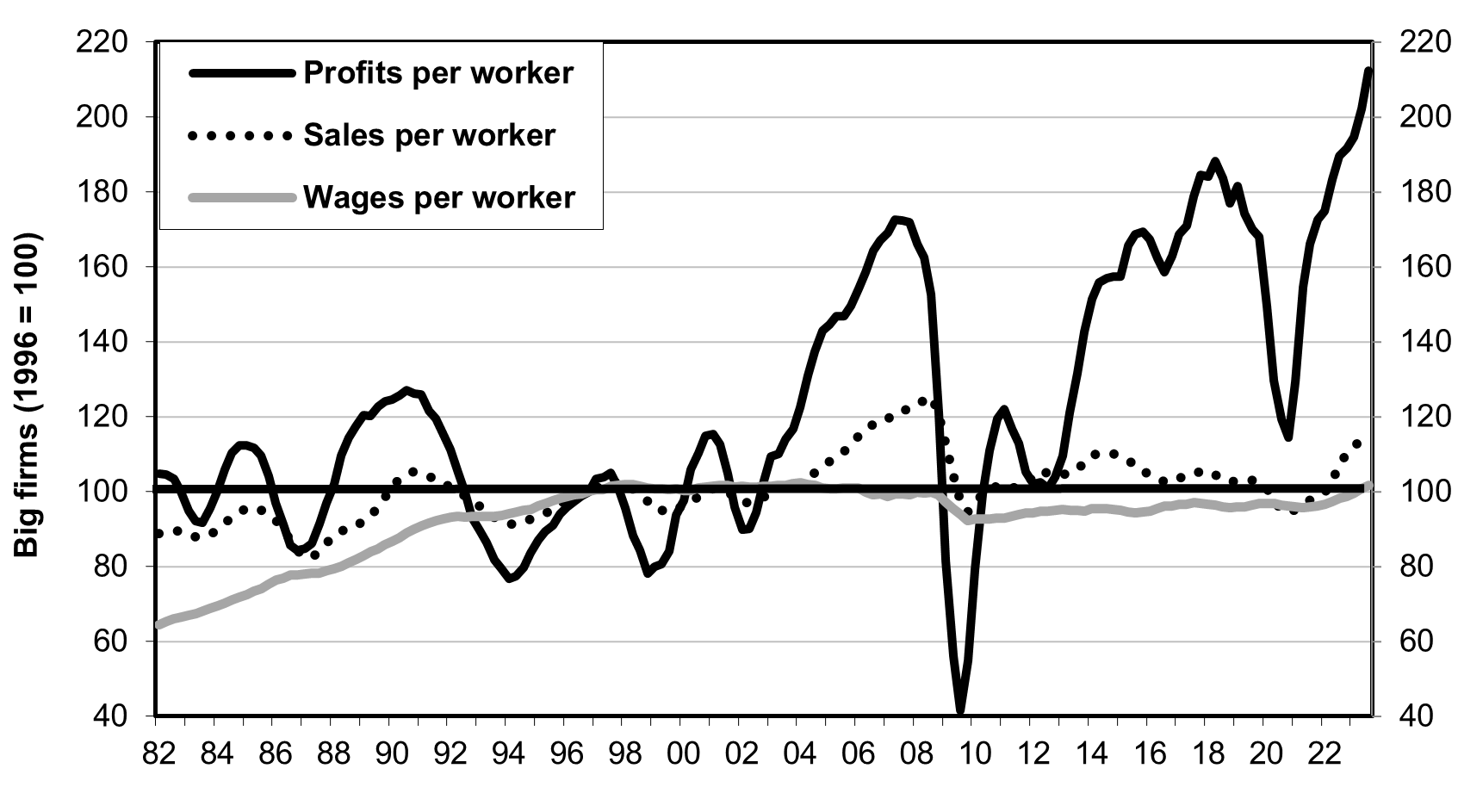

Stock prices are supposed to reflect both current profits and expectations about future profits. However, while investor sentiment and prices should incorporate how those profits are earned—because it affects their sustainability—they do not necessarily do so. In Japan, profits have grown even as the economy soured. Profits, in turn, should reflect some combination of rising sales and improvements in company efficiency. But in Japan, they do not. From 1996 to 2023, profits per worker among Japan’s 5,000 largest firms more than doubled (up 110%). However, sales per worker were up only 12%. Worse yet, nominal compensation (wages plus benefits) per worker was up just 1% over nearly three decades (see chart below). There are about 4,000 firms listed on the stock market, so these 5,000 are a good approximation.

Source: https://www.mof.go.jp/english/pri/reference/ssc/historical/all.xls

As I discussed in a previous post, if wages are stagnant, someone else has to make up for the missing consumer demand. In Japan, it’s year after year of government deficits, near-zero interest rates for nearly a quarter century, and an excessively weak yen to boost exports.

One of the best measures of company productivity is called Returns on Assets (ROA), i.e. how much operating profit a firm earns for every yen of tangible and financial assets. For example, Tesla gets more profit out of $1 billion worth of factory space and equipment and financial assets than does Chrysler. During the lost decades, ROA for the 5,000 biggest companies dropped to an average of 3.5% during 1994-2023. Despite claims that corporate governance reforms would raise efficiency, that has not happened, at least not yet. ROA in 2023 was no better than in the mid-1990s (see chart below). In my opinion, while improved governance may help shareholders get their share of the profits, competition is a far more powerful force when it comes to improving performance.

The Big New Driver: Stock Buybacks Used To Artificially Raise Prices

Beyond wage suppression, companies are now using financial shenanigans to boost prices: a record level of buying back their own shares. In some situations, stock buybacks can serve a useful purpose, but this is not one of them. I’ll be using a bit of jargon, but I’ll explain, so please bear with me,

The best measure of the value of a stock is what is called the price-earnings (PE) ratio. That’s the price of one share of stock compared to company profits (earnings) per each share of stock. In the US, as of December 31st, the PE ratio was about 22, in Japan about 16, and in Germany, 15. Let’s take 20 for our example since it makes the arithmetic easier. If a company has issued 1 million shares and its profits are $1 million, then earnings are $1 per share. At a 20 PE ratio, the stock price would be $20. Since the price is also supposed to reflect future profits, a fast-growing company might deserve a PE of 25 while a slower-growing company might have a ratio of 15.

Let’s look more closely at the key factor of earnings per share, also known as Return on Equity (ROE). There are two ways to increase ROE from $1 per share to $2. The hard way is to double total earnings from $1 million to $2 million, The easy way for a cash-rich company is to buy back its own shares and thereby lower the number of shares by half. In that case, even though total profits have not improved at all, profits per share have now doubled. The same $1 million in profit is now divided by just 500,000 shares and so equals $2 per share. That easy road is the one now being taken by so many Japanese firms.

In 2023, a record 992 companies announced share buybacks for a near-record ¥10 trillion ($67 billion). And it would not be surprising if the number rose in 2024. Honda announced it would buy back 4% of its outstanding shares in just one year. Some firms do this year after year. And not just in Japan

When investors see companies using this technique to boost their share price, they jump in to reap the advantage, which lifts the price even more. One of them was famed investor Warren Buffet, who purchased about 5% of the shares in Japan’s top five trading companies. Buffet told the Nikkei, “If they are repurchasing their shares, we generally regard that as a plus. We like the idea of the number of shares going down.” Foreign investors comprised about a third of the net purchases of Japanese stocks in 2023.

Behind The Buybacks: Pressure From Stock Exchange Management

The recent rally is due to an increase in both actual and anticipated buybacks as a result of new rules issued by the Japan Exchange for the 1,840 companies in the most elite “Prime” Section of the Exchange. The rules go into effect in March 2025 but companies need to move now to prepare for the shift. One of the requirements is that companies with a low price—a so-called price-to-book-value ratio (PBR) below 1.0—announce their steps (or lack of such) to improve their price to a ratio above 1.0. About half of these “Prime” companies suffer from a PBR below 1.0.

A PBR below 1.0 tells you that investors do not see the company as able to grow. Here’s why. The book value is the value of a firm’s net assets, i.e. its assets minus its liabilities (what it owes to others). If the PBR is below 1.0, that means that the amount of cash a company could rake in just by dissolving itself, paying off the debt, and selling the assets piece by piece is more than its total value as an ongoing firm. The market is expecting the company to perform so badly that it destroys value. Some are just poor performers. Others are firms with superb technical prowess whose revenue has been demolished by market changes. Famous camera maker Nikon has a PBR below 1.0 because the rise of smartphones has decimated the camera market. Revenue peaked at ¥1 trillion in 2013, and was down by more than a third, to ¥628 billion, as of 2023. It is trying to write a new future for itself in different products. Revenues for the more diversified Canon are no higher than way back in 2006 and its PBR is a bit above 1.0.

Another reason for a low PBR is that so many companies hoard fallow cash that they cannot invest profitably. Yet, they have not returned this cash to shareholders who might invest the money in better companies. One measure is called “net cash.” Not only are their total assets higher than their liabilities—as in any bankruptcy company—but even their simple financial holdings are larger than their total liabilities. For the 1,840 companies in the Prime Section, their net cash averages 20% of their total market value, compared to 7% in Europe and 3% in the US. So, they are being pressured to use the cash to buy back shares, and thereby lift its price.

Do Stock Buybacks Constitute Reform?

Many analysts see relieving corporations of fallow cash as a positive move and so do I. Fallow cash is one of the factors holding down ROA. Others see stock buybacks as improving shareholder value, which they falsely equate with corporate performance.

What counts most for Japan’s overall economy is how the sellers invest the cash that they gain from such sales. Foreigners hold almost a third and they shift between being net buyers and net sellers of Japanese stocks; so this does not necessarily help Japan. Only 13% of stocks and Investment Trusts (mutual funds) are owned by households in Japan, compared to 45% in the US and 28% in Europe. So, this will not result be much of a boost to consumer spending. Will the remaining half of investors hoard the cash, or invest it in firms with better growth prospects, or use it to buy overseas companies? All that remains to be seen.

P.S. I’ve been told by the Economist that, to listen to the interview with me on Economist.com’s “Money Talks,” on the “Japan is Back” story as well as how Japan can get back its innovation mojo—you can sign up for a free trial of Economist Podcasts and then cancel after listening. Alternatively, I logged out of my account and then clicked Click here, and the podcast came on. I’m at minute 21:55. Let me know how it works for you.

You have been mentioned in a recent article I read, congrats

https://www.scmp.com/comment/opinion/article/3250598/pumped-stock-markets-are-no-indication-countrys-economic-health

I was genuinely inspired by your talk and created a brief trailer of your Economist interview, including links to the full podcast and your book. You can view it here: https://www.youtube.com/watch?v=SyO4i7yjMPU.

It's currently unlisted, and if you'd prefer it not be shared, just let me know and I'll remove it immediately.