¥144 Is Weakest Since Last November

Yen Follows Rate Gap As Markets Now Take BOJ and US Fed At Their Word

Source: https://www.federalreserve.gov/releases/h10/hist/dat00_ja.htm, https://www.federalreserve.gov/datadownload/Choose.aspx?rel=H15, and https://www.wsj.com/market-data/quotes/bond/BX/TMBMKJP-10Y

As I write this, the yen stands at ¥143.8/$. That’s the weakest it has been since November 19th, about a month before the Bank of Japan (BOJ) “tweaked” its interest rate policy to allow 10-year Japan Government Bonds to rise to a maximum of 0.5%. Following that move, which the market misinterpreted as the first of many hikes in interest rates, the yen strengthened to ¥127 in January. Many forecasters projected it could continue to strengthen. Instead, it started steadily creeping back upwards.

As we’ve repeatedly stated, over the past two years, the ¥/$ rate has closely tracked the gap between Japanese and American 10-year government bond rates, with a supremely high 97% correlation. The bigger the gap, the weaker the yen (see chart at the top). Earlier in the year, many market players believed that the gap would lessen as the BOJ raised interest rates and the Fed began cutting them toward year’s end. Now, far fewer market participants still believe that; so fewer are willing to buy the yen at prices as high as they were a few months ago. The decreased demand for the yen causes it to weaken.

Learning to Believe the Central Banks Mean What They Say

On the BOJ side, even though Governor Haruhiko Kuroda made it clear that the move on 10-year bond rates was just loosening a “steam valve,” a tactic aimed at enabling him to maintain the BOJ’s ultra-dovish policy, many in the market believed he would be forced to raise rates. Some even believed he intended to raise rates but did not want to say so. Then, when Kuroda finished his term and was replaced by Kazuo Ueda, the market view was that Ueda would move rates higher in response to higher-than-expected inflation. Many players did not believe him when he said that BOJ still saw today’s inflation as temporary, that sustainable inflation required 3% nominal wage hikes, and that lifting rates too soon was a worse mistake than lifting them too late. Now, they increasingly believe he means what he says and that he has the ability to sustain his policy until the picture becomes clearer.

As for the Fed, many forecasters expected that the Fed’s campaign of raising would send the US into recession sometime this year and that, as a result, the Fed would have to start cutting rates again before the year ended. Instead, the US economy has proved surprisingly resilient in the face of higher interest rates and, as a result, Fed chair Jerome Powell told Congress this week that he foresees two more interest rate hikes this year. Unless the economy weakens, bringing inflation back down to the Fed’s goal of 2% will prove difficult.

With the BOJ keeping rates low and the Fed raising them again, the US-Japan rate gap has rebounded. As it did so, the yen/$ rate weakened in tandem (see again chart at the top).

A Chronically Weak Yen

While the interest rate gap has been the single-biggest factor in the yen/$ rate in the short term, the more fundamental determinant has been the increasing loss of competitiveness on the part of many of Japan’s leading companies. As a result, it takes a weaker and weaker yen for Japanese companies to sustain exports.

The best measure of the yen’s underlying value is the so-called “real yen,” which adjusts the yen’s nominal value for changes in inflation/deflation in Japan compared to other countries. That tells us the real purchasing power of the yen: how many cars or computer chips does Japan have to send to foreign buyers in order to pay for all the coal and wheat it imports? If it has to pay more in the form of cars or computer chips to buy the same amount of coal and wheat, it means the real yen is weaker because Japan’s exporters are less competitive than they used to be. According to this measure, Japan’s real yen is the weakest it has been since a half-century ago in the early 1970s (see chart below).

Source: https://www.stat-search.boj.or.jp/ssi/cgi-bin/famecgi2?cgi=$graphwnd_en

Note: The horizontal line at 100 is the 1970-2023 average. The bands at 80 and 120 show there the real yen has been about two-thirds of the time. It further illustrates how weak today’s yen is.

The benefit of a weak currency is that it is supposed to help a country export more, while it imports fewer products that compete with domestic producers. This should boost domestic growth. So far, however, this has not proved to be the case. The real, i.e., price-adjusted, trade deficit is much higher than it was two years ago (see chart below).

Source: https://www.esri.cao.go.jp/jp/sna/data/data_list/sokuhou/files/2023/qe231_2/tables/gaku-jk2312.csv

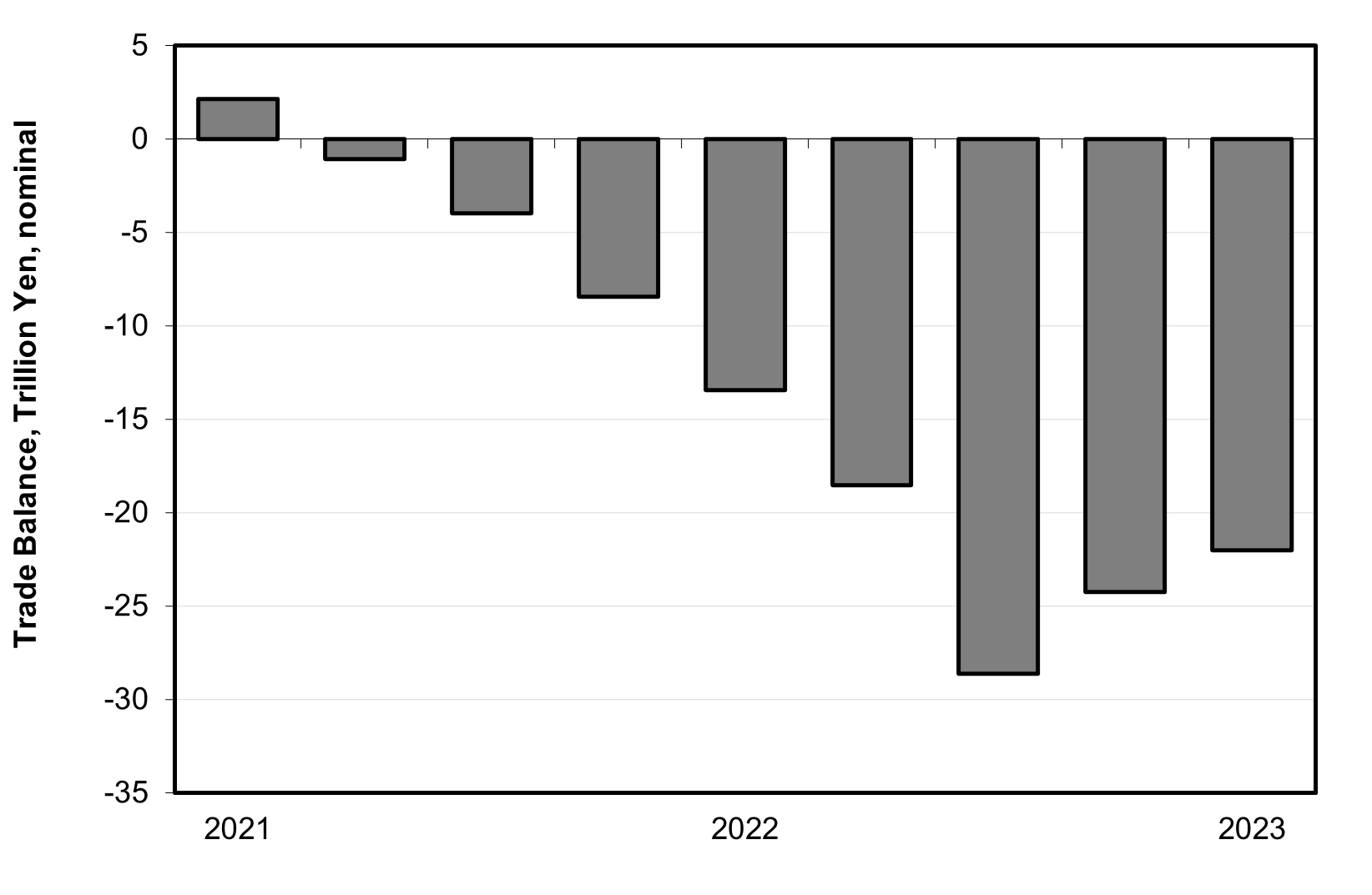

At the same time, the nominal trade deficit has deteriorated to around 4% of GDP as of January-March (see chart below).

Source: https://www.esri.cao.go.jp/jp/sna/data/data_list/sokuhou/files/2023/qe231_2/tables/gaku-mk2312.csv

In other words, Japan is paying higher prices for needed imports of raw materials, energy, foodstuffs, machinery, and assorted consumer goods. This is one of the major reasons for the rise in consumer inflation and the corresponding drop in real wages. In essence, the weak yen is transferring income from Japanese consumers to foreign producers as well as to Japanese exporters. Japanese households are paying a high price for little benefit.

Wither the Yen?

What does all this tell us about the future value of the yen? Back in 2001-13, when the interest rate gap between the US and Japan was 3%, it took just 110 yen to buy a dollar. Today, by contrast, when the rate gap is 3%, Japan has to pay around 130 yen to buy a dollar (see chart below). ). It looks like, no matter what happens with interest rates, the yen will remain a lot weaker than it was a couple decades ago—at least for a long while.

Source: https://www.federalreserve.gov/releases/h10/hist/dat00_ja.htm, https://www.federalreserve.gov/datadownload/Choose.aspx?rel=H15, and https://www.wsj.com/market-data/quotes/bond/BX/TMBMKJP-10Y

Interesting, thanks for sharing. Have you notice the Yen and Gold rally together during times of panics?

Thanks for sharing another thoroughly researched article. Are similar factors at play regarding the JPY/ Euro fx rates?